Markets Scramble as Macro Data Looks to Upend the Risk-On Run

Synopsis

This week’s Lenses highlights mounting macro uncertainty as hedge funds unwind crowded trades and volatility picks up across inflation and rate-sensitive themes. Healthcare remains a rare bright spot, balancing defensive appeal with policy risk, while the rally narrows around a few megacap winners. With cyclicals struggling to stage a true comeback and investors cautious ahead of September’s Fed meeting, markets remain fragmented, demanding agility and selective conviction.

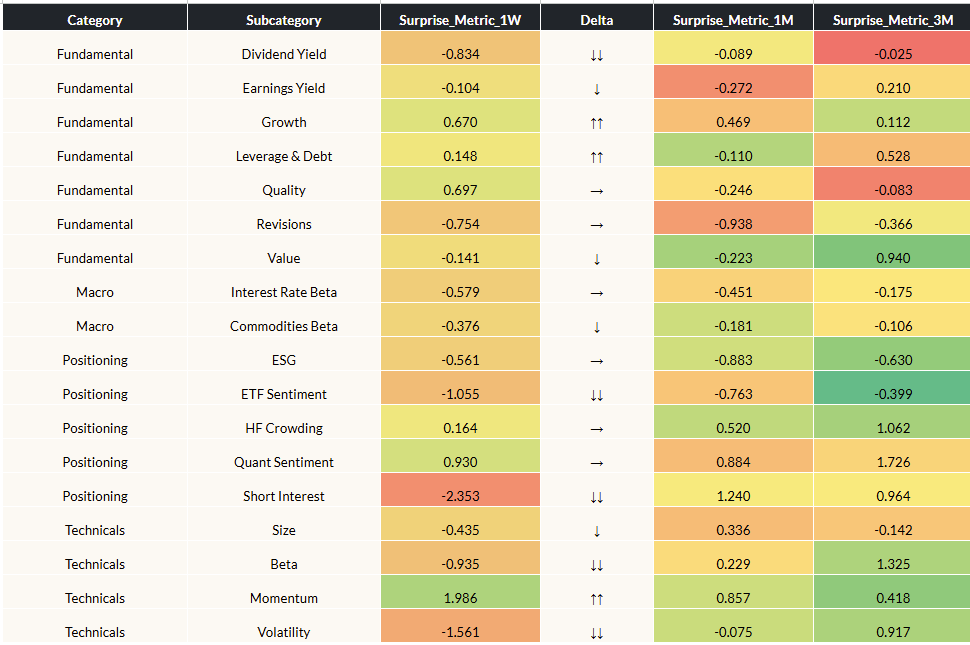

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 08/01/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Quality outperformed for the second week, signaling a possible structural shift after prolonged weakness. Weaker-than-expected jobs data and negative prior month revisions spooked investors, highlighting labor market fragility and driving equities lower while bonds rallied. Meanwhile, surprise inflation has further complicated the Fed’s path ahead of September. How Quality performs in the coming weeks will be an important signal for whether risk-off behavior returns after being sidelined in Q2/Q3

- Momentum and Growth showed significant improvement this week off Q2 megacap earnings from Microsoft and Meta fueling gains. However, Beta and Volatility lagged behind—underscoring that the increasing divide between a handful of big winners versus broad-based participation. This growing concentration suggests that, while the largest names continue to outperform, the broader risk-on rally may be losing steam as gains become more narrowly focused.

- Institutional rotation persisted, with ETF, Short Interest, and Crowding factors all falling sharply likely due to further de-risking in lieu of recent macro data surprises—such as weak jobs numbers and sticky inflation. The continued shift suggests that institutional investors are unwinding consensus trades and adopting a more cautious stance as we move beyond Q2 earnings and head into late Q3/Q4.

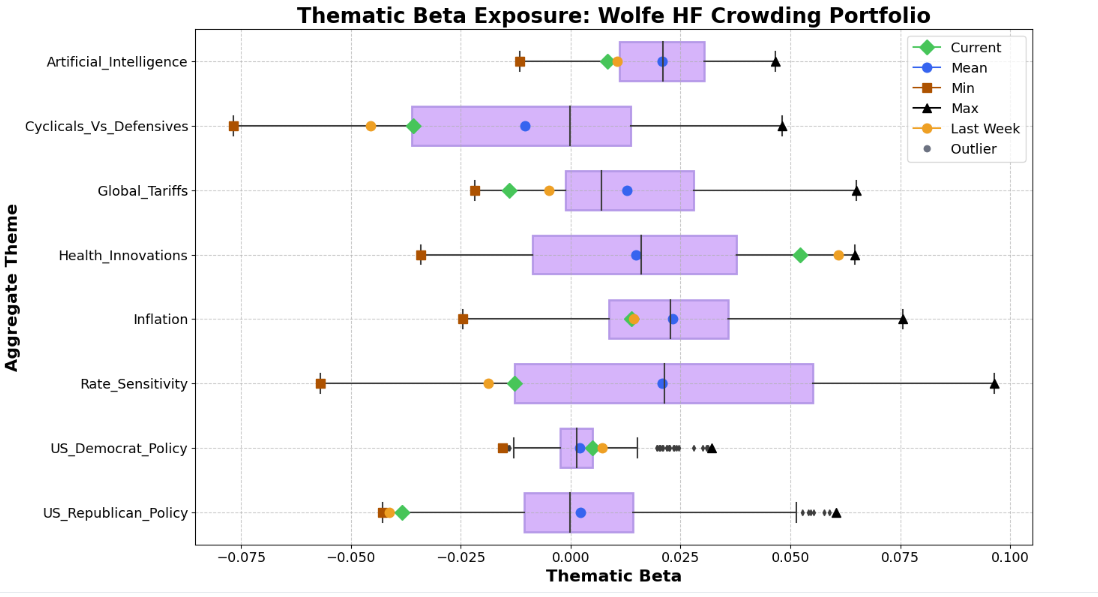

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024. How to read this graph

Highlights

- Health Innovations ticked down but remain a favored theme in hedge fund portfolios. The sector likely faced some pressure after Trump’s letters targeting pharma prices, yet funds seem to still seek alpha in healthcare’s defensive qualities and strong innovation trend in drug and biotech pipelines.

- Rate Sensitivity and Inflation themes are set to take center stage in Q3/Q4 as new Trump tariffs, persistent inflation, and labor market softness add complexity to the Fed’s path. With forward guidance now more uncertain, expect these themes to remain volatile as investors reposition in the coming weeks.

- Cyclicals vs. Defensives continues to show a modest shift toward risk, but it’s too soon to call a full rebound. Ongoing policy uncertainty and mixed macro signals may keep risk capital cautious until September’s data and Fed meeting provide clearer direction for the rest of the year.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

- Are we prepared for persistent volatility in crowded trades? With hedge funds and ETFs unwinding popular positions amid macro shocks, are we ready to capitalize on dislocations while avoiding drawdowns in consensus trades?

- Is the rotation between cyclicals and defensives sending a false signal? As positioning turns modestly bullish but macro headwinds persist, are we at risk of chasing a rebound too early—or should we stay patient for more clarity post-September Fed?

- Are we positioned for healthcare’s defensive alpha or potential policy setbacks? With ongoing innovation supporting the sector but renewed political pressure on drug pricing, are we balancing healthcare exposure to capture upside while mitigating regulatory risk?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses, we explore markets that are no longer rewarding broad risk-taking, as policy uncertainty, tariffs, and structural rate pressures are raising volatility and dispersion across assets. In this regime, alpha comes from selectivity—favoring quality balance sheets, value over duration-sensitive growth, controlled rate exposure, and idiosyncratic themes like health innovation rather than index-level beta. In short, discipline and discrimination matter more than conviction on the macro path.

This week’s Lenses highlights a market leaning back into risk even as underlying fragilities persist. Institutions are selectively rotating toward cyclicals, and tentatively re-embracing AI—but each theme carries asymmetric risks tied to policy timing, late-cycle dynamics, and unproven profitability.

This week’s Lenses highlights a gradual return of risk appetite, with rate-sensitive trades, cyclicals, and even short-squeeze names showing renewed strength. Yet record highs in gold, flat performance in Technicals, and unresolved tariff risks underscore that this rotation remains tentative...