Cautious re-risking takes hold, but fragile macro undercurrents keep markets on edge

Synopsis

This week’s Lenses highlights a gradual return of risk appetite, with rate-sensitive trades, cyclicals, and even short-squeeze names showing renewed strength. Yet record highs in gold, flat performance in Technicals, and unresolved tariff risks underscore that this rotation remains tentative. The throughline: investors are cautiously re-risking, but fragile macro undercurrents demand discipline in positioning.

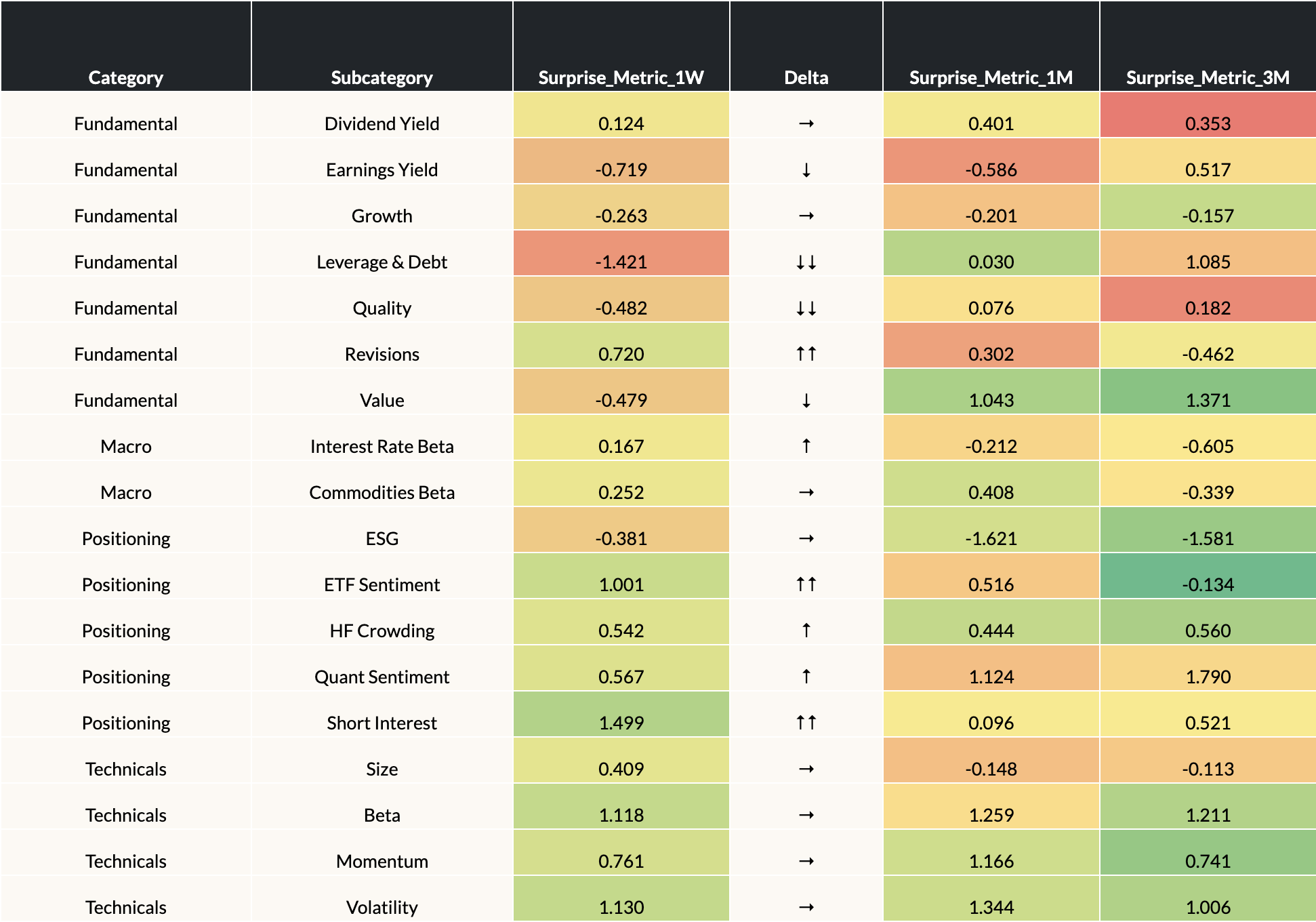

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 9/19/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Factors signal a murky risk backdrop. Quality and Leverage sold off in tandem—an unusual move that, alongside modest Growth and Value declines, underscores market skepticism around the Fed’s rate cut. With labor data now the swing variable for the pace of easing, expect higher volatility around upcoming macro releases.

- Positioning reveals speculative undercurrents. Gains in Short Interest and ETF sentiment suggest squeeze-driven rallies and tactical buying are still at play. Meanwhile, gold’s record highs point to mounting concerns over debt sustainability and sticky inflation—implying portfolios may need hedges beyond equities.

- Technicals steady, but cracks could emerge beneath consumer resilience. Market breadth remains narrow with Tech driving leadership, while flat technicals hint at fading momentum. Strong retail sales mask a softening labor backdrop, raising the risk that consumer demand—and with it, cyclical exposure—could weaken in the months ahead.

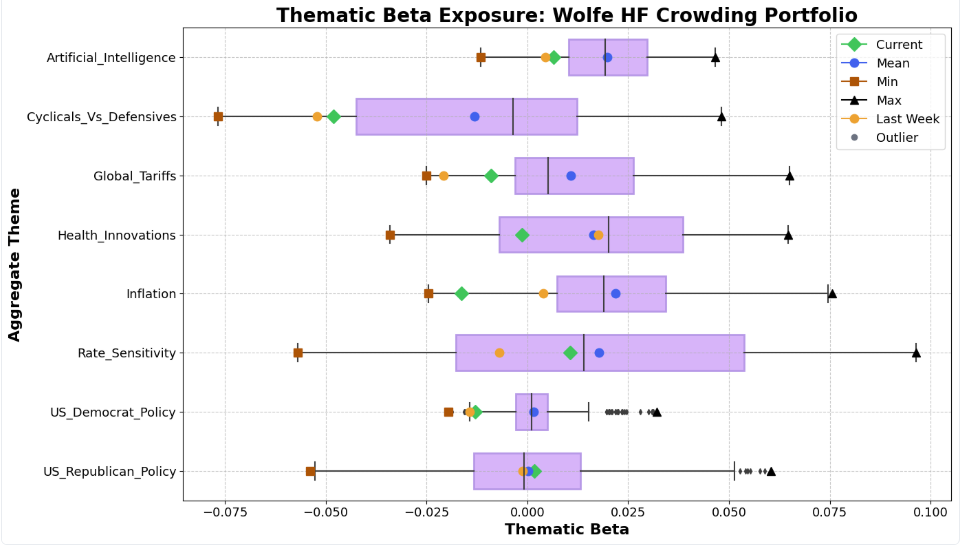

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Rate sensitivity climbs, inflation fears ebb. The modest rebound in rate-sensitive factors shows investors tiptoeing back into duration trades, while softer inflation signals should keep the Fed’s easing path intact. Positioning is still below historical norms though, implying there’s room for further upside if rate-cut conviction strengthens.

- Cyclicals vs defensives edge higher. The risk-on focused theme ticked up, hinting at institutions gradually rotating out of caution. It’s not yet a wholesale shift, but the steady trickle suggests risk appetite is rebuilding—and could accelerate if macro data confirm a soft landing.

- Tariff theme steadies, but policy risk lingers. Hedge fund exposure remains contrarian, though recent moves by Turkey and Switzerland to ease trade tensions offered a modest lift. With India–U.S. negotiations unresolved, the risk of higher import costs feeding inflation looms large—making tariff outcomes a key macro swing factor for portfolios.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

Are rate-sensitive trades signaling conviction—or just early positioning?

With Rate Sensitivity ticking higher but still below historical norms, are investors steadily building exposure to an easing cycle, or simply testing the waters ahead of labor data that could reshape the Fed’s path?

Is the return of risk appetite durable—or speculative froth?

Short Interest rallies and cyclical gains point to re-risking, but much of it looks squeeze-driven. Will this cautious optimism evolve into a sustainable rotation, or fade once macro volatility resurfaces?

Will tariff relief offset inflation pressures—or prolong uncertainty?

Turkey and Switzerland have moved to ease U.S. trade frictions, yet India–U.S. negotiations remain unresolved. Are portfolios prepared for tariff policy to either soften inflation headwinds—or reignite cost pressures that undercut the easing cycle?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses, we explore markets that are no longer rewarding broad risk-taking, as policy uncertainty, tariffs, and structural rate pressures are raising volatility and dispersion across assets. In this regime, alpha comes from selectivity—favoring quality balance sheets, value over duration-sensitive growth, controlled rate exposure, and idiosyncratic themes like health innovation rather than index-level beta. In short, discipline and discrimination matter more than conviction on the macro path.

This week’s Lenses highlights a market leaning back into risk even as underlying fragilities persist. Institutions are selectively rotating toward cyclicals, and tentatively re-embracing AI—but each theme carries asymmetric risks tied to policy timing, late-cycle dynamics, and unproven profitability.

This week’s Lenses highlights mounting macro uncertainty as hedge funds unwind crowded trades and volatility picks up across inflation and rate-sensitive themes. Healthcare remains a rare bright spot, balancing defensive appeal with policy risk, while the rally narrows around a few megacap winners. With cyclicals struggling to stage a true comeback and investors cautious ahead of September’s Fed meeting, markets remain fragmented, demanding agility and selective conviction.