Broadening Risk-On Rally Drives Rotation Into Value, Policy Winners, and Speculative Plays

Synopsis

This week’s Lenses highlights a broadening risk-on rally as investors rotate into value and policy-driven sectors, push up the risk curve with speculative activity, and move beyond crowded macro trades, signaling a recalibration of exposures ahead of key market catalysts.

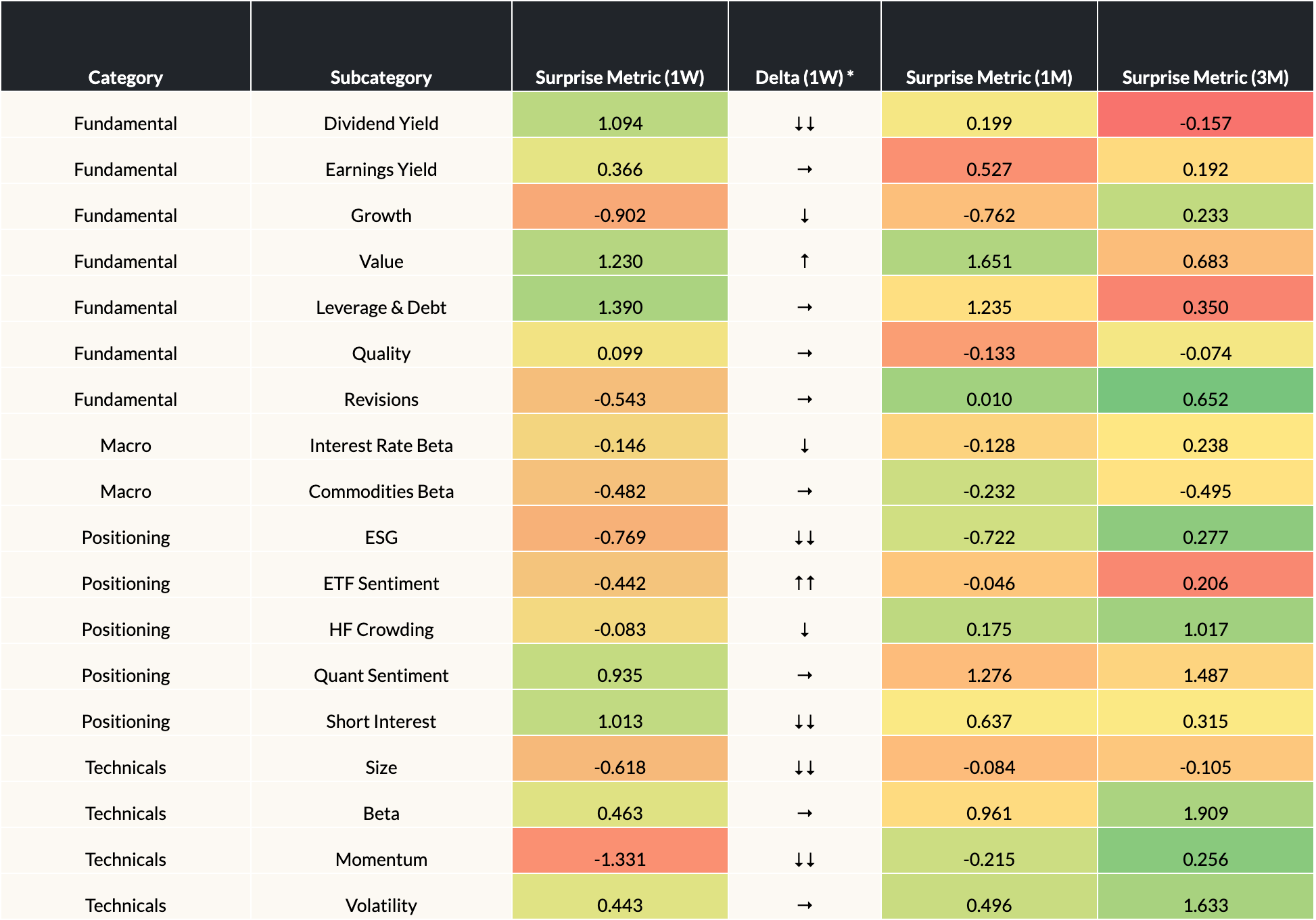

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 7/7/2025

*Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Cyclical rotation continues to lift Value and pressure Growth.

Value and Leverage & Debt factors posted strong positive 1W surprises, reflecting renewed optimism and outperformance in cyclicals like Financials and Energy. Meanwhile, Growth continued to lag amid interest rate and valuation pressures—reinforcing the value of diversifying across equity styles to better manage shifting market risks. - Speculative Surge in Shorted Stocks Raises Caution Flags

Short Interest experienced another strong positive 1W surprise, signaling aggressive buying in heavily shorted names and speculative risk taking. Escalating froth evidenced by this factor’s continued rally could leave markets more vulnerable to sharp pullbacks or deeper corrections if sentiment reverses. - Broader Participation as Momentum and Size Weaken

Continued negative surprises in Momentum and Size this week point to investors rotating out of crowded leaders and toward a more evenly distributed risk rally. Small caps may also benefit further from policy changes like the Big Beautiful Bill, but the overall shift underscores the importance of monitoring where new leadership emerges.

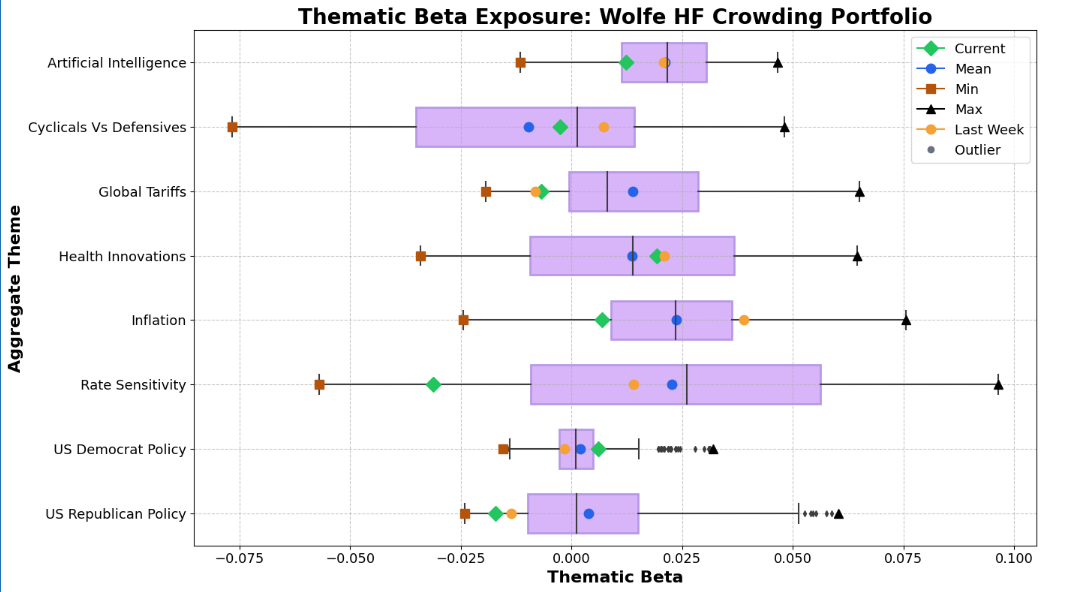

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Inflation and Rates Themes Lose Momentum

Betas for inflation and rate-sensitive themes dropped sharply after last week’s strength, as last week’s tight labor data dampened hopes for imminent rate cuts. Expect heightened volatility in these exposures as market expectations evolve ahead of the September Fed meeting. - Democratic Policy Beta Rises on Legislative Tailwinds

Democratic Policy themes gained traction, boosted by the Big Beautiful Bill’s provisions supporting Renewable Energy, Transportation, and other “Build Back Better” sectors—driving renewed investor focus on policy beneficiaries. - AI Theme Volatility Persists Amid Uncertainty

The AI thematic beta has fallen back near its 25th percentile, reflecting ongoing whipsaw action. Geopolitical tensions, Q2 earnings, and emerging low cost AI competition continue to inject uncertainty, and will likely keep hedge fund allocations in flux.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

- Are we positioned to benefit from the ongoing cyclical rotations, while managing style risk?

With Value and Leverage outperforming and Growth, Momentum, and Size under pressure, does our equity mix capture upside in cyclicals and small caps, while maintaining enough diversification to weather a potential reversal in leadership? - How are we balancing opportunity and risk amid rising speculation and shifting macro themes?

Given the surge in speculative buying of shorted stocks and the fading influence of inflation and rate-sensitive trades, are our risk controls robust enough to guard against sharp reversals or volatility spikes as we approach key policy milestones? - Do we have adequate exposure to evolving policy and thematic trends?

As Democratic policy themes gain traction and AI sector volatility persists, are we capturing new opportunities in policy beneficiaries like Renewable Energy and Transportation, while staying agile in sectors experiencing rapid sentiment shifts?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses, we explore markets that are no longer rewarding broad risk-taking, as policy uncertainty, tariffs, and structural rate pressures are raising volatility and dispersion across assets. In this regime, alpha comes from selectivity—favoring quality balance sheets, value over duration-sensitive growth, controlled rate exposure, and idiosyncratic themes like health innovation rather than index-level beta. In short, discipline and discrimination matter more than conviction on the macro path.

This week’s Lenses highlights a market leaning back into risk even as underlying fragilities persist. Institutions are selectively rotating toward cyclicals, and tentatively re-embracing AI—but each theme carries asymmetric risks tied to policy timing, late-cycle dynamics, and unproven profitability.

This week’s Lenses highlights a gradual return of risk appetite, with rate-sensitive trades, cyclicals, and even short-squeeze names showing renewed strength. Yet record highs in gold, flat performance in Technicals, and unresolved tariff risks underscore that this rotation remains tentative...