Markets Re-Risk into FOMC Week, but Safety Net is Thinning

Synopsis

This week’s Lenses highlights a market leaning back into risk even as underlying fragilities persist. Institutions are selectively rotating toward cyclicals, and tentatively re-embracing AI—but each theme carries asymmetric risks tied to policy timing, late-cycle dynamics, and unproven profitability. The common thread: investors are willing to chase opportunity, but the margin for error is narrowing, making disciplined positioning more important than outright bullishness.

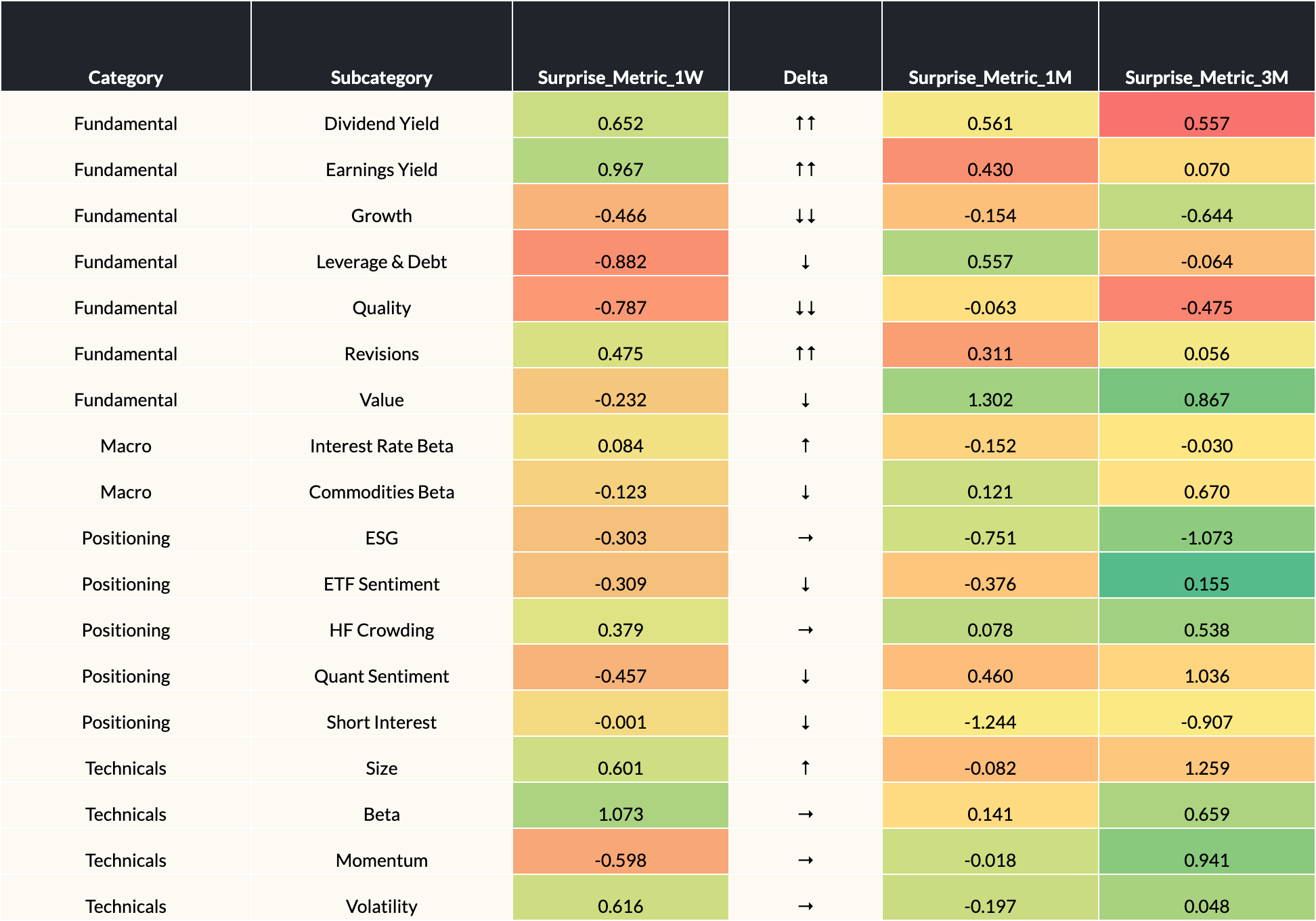

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 12/5/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Mixed macro signals are keeping uncertainty elevated, even as markets lean dovish. Jobless claims hit cycle lows while ADP showed job losses, and inflation data sent conflicting signals (core PCE easing vs. ISM Prices Paid at highs). The macro fog reinforces late-cycle dynamics in which investors should stay selective and avoid over-interpreting any single datapoint.

- A confident Fed-cut narrative is boosting risk sentiment—but asymmetric policy risk remains. Markets appear convinced the Fed will deliver a 25 bp cut, lifting Beta, Vol, Size, and helping Tech stabilize. But Growth, Leverage, and Quality factors still lag, and the bar for further 2026 easing is increasingly high. A policy disappointment post-meeting could trigger rotation back into defensives like Quality and Earnings Yield.

- Equities’ easing narrative contrasts sharply with bond-market stress, keeping duration risk elevated. Despite 150 bps of cuts, Treasury yields have risen on sticky inflation, higher term premia, and worsening fiscal deficits. If these pressures persist, duration is likely to underperform, strengthening the case for refined hedging and cross-asset risk management.

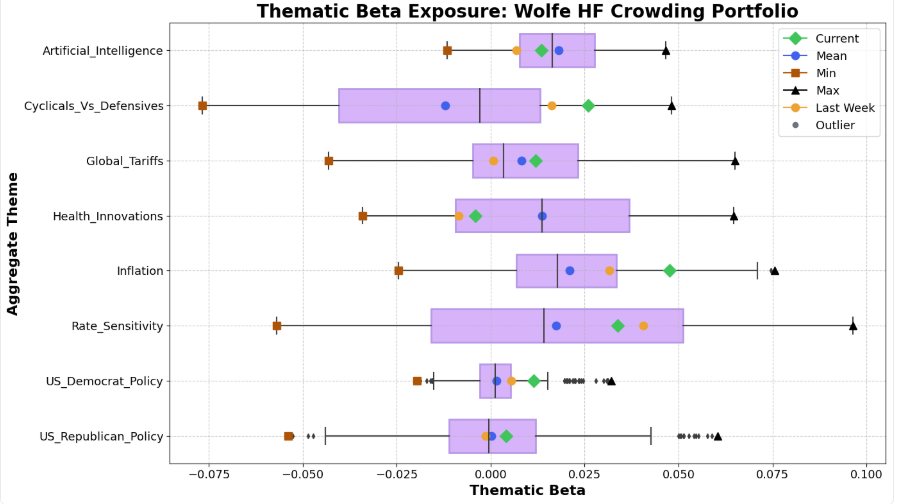

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Inflation-sensitive assets are seeing renewed institutional interest, but the case for major reallocations remains limited. Beta shifts suggest increased exposure to inflation hedges, as markets price moderate long-term inflation (2.2 -- 2.4% BEIs) and elevated short-term risks (>3%). With outsized inflation surprises still a low-probability tail risk, investors should stay vigilant but avoid over-rotating into expensive real-asset hedges.

- Cyclical leadership continues to build under a dovish rate backdrop, supporting selective risk-taking. Cyclicals vs. Defensives keeps rising, and expectations heading into the FOMC have pulled flows back into Tech and Energy, while Healthcare cooled after a strong run. The backdrop favors maintaining cyclical exposure—but doing so with an eye on late-cycle fragility and policy-driven volatility.

- AI remains a mild portfolio positive, but bubble-risk is rising as capex outpaces proven profitability. The recent rally reflects renewed enthusiasm, yet debt-funded AI infrastructure spending has accelerated faster than demonstrable returns. A future profit shortfall could trigger cascading effects—an AI-equity drawdown, a hit to wealth effects, and spillovers into broader economic activity—making valuation discipline critical.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- How durable is the current re-risking as the cycle turns late?

Cyclical leadership and renewed interest in Tech and AI suggest improving sentiment, but the sustainability of this rotation hinges on policy follow-through and whether growth can absorb higher real yields and persistent fiscal pressures. - Are investors underestimating the tail risks around inflation and policy?

While long-term BEIs remain anchored, sticky short-term pricing and rising term premia imply inflation risk isn’t fully behind us—raising the question of whether institutions are taking on too much exposure to assets sensitive to policy disappointment. - Is AI enthusiasm outrunning fundamental profitability?

The mild rebound in AI plays masks deeper concerns about debt-funded capex, uncertain margins, and the potential for a wealth-effect reversal if profits disappoint—making it critical to assess whether the AI trade is becoming a crowded, high-beta liability.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses, we explore markets that are no longer rewarding broad risk-taking, as policy uncertainty, tariffs, and structural rate pressures are raising volatility and dispersion across assets. In this regime, alpha comes from selectivity—favoring quality balance sheets, value over duration-sensitive growth, controlled rate exposure, and idiosyncratic themes like health innovation rather than index-level beta. In short, discipline and discrimination matter more than conviction on the macro path.

This week’s Lenses highlights a gradual return of risk appetite, with rate-sensitive trades, cyclicals, and even short-squeeze names showing renewed strength. Yet record highs in gold, flat performance in Technicals, and unresolved tariff risks underscore that this rotation remains tentative...

This week’s Lenses highlights mounting macro uncertainty as hedge funds unwind crowded trades and volatility picks up across inflation and rate-sensitive themes. Healthcare remains a rare bright spot, balancing defensive appeal with policy risk, while the rally narrows around a few megacap winners. With cyclicals struggling to stage a true comeback and investors cautious ahead of September’s Fed meeting, markets remain fragmented, demanding agility and selective conviction.