Macro Uncertainty, Micro Alpha

Synopsis

In this week’s Lenses, we explore markets that are no longer rewarding broad risk-taking, as policy uncertainty, tariffs, and structural rate pressures are raising volatility and dispersion across assets. In this regime, alpha comes from selectivity—favoring quality balance sheets, value over duration-sensitive growth, controlled rate exposure, and idiosyncratic themes like health innovation rather than index-level beta. In short, discipline and discrimination matter more than conviction on the macro path.

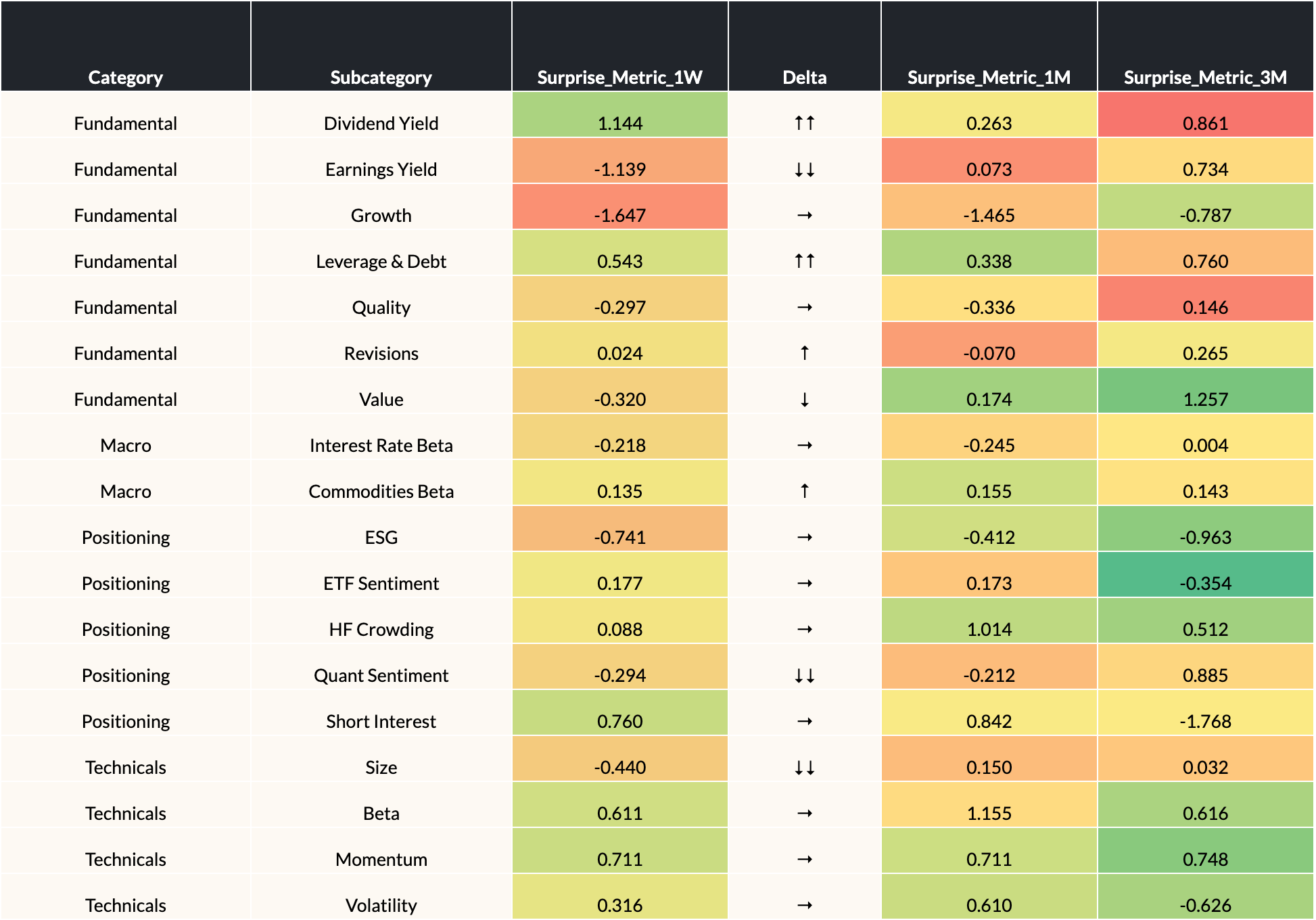

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 1/16/2026

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Policy uncertainty is re-pricing rates volatility and factor leadership. Shifting odds in the Fed chair race have injected uncertainty into the policy path, driving higher rate volatility and continuing to pressure pro-cyclical factors (Momentum, High Beta, Vol control). In contrast, Value’s sensitivity to higher real-rate dispersion and steeper curves continues to support its relative outperformance versus Growth, reinforcing the durability of the 2025 regime.

Small-cap leadership is growth-optimistic but balance-sheet fragile. Recent small-cap strength signals improving domestic growth expectations, but the trade is increasingly contingent on easier financial conditions. With rate-cut expectations for 2026 still up in the air, and a large share of small-cap debt rolling in 2025–26, higher interest expense risk undermines earnings leverage, arguing for selective exposure rather than broad Size factor beta. - Tariff-driven geopolitics add a new tail risk to risk assets. The U.S. move to impose tariffs on EU countries over Greenland elevates trade and retaliation risk, with export-intensive industries, global cyclicals, and firms with transatlantic revenue exposure most vulnerable. This backdrop favors a more defensive tilt within cyclicals and a higher premium on pricing power and domestic revenue exposure.

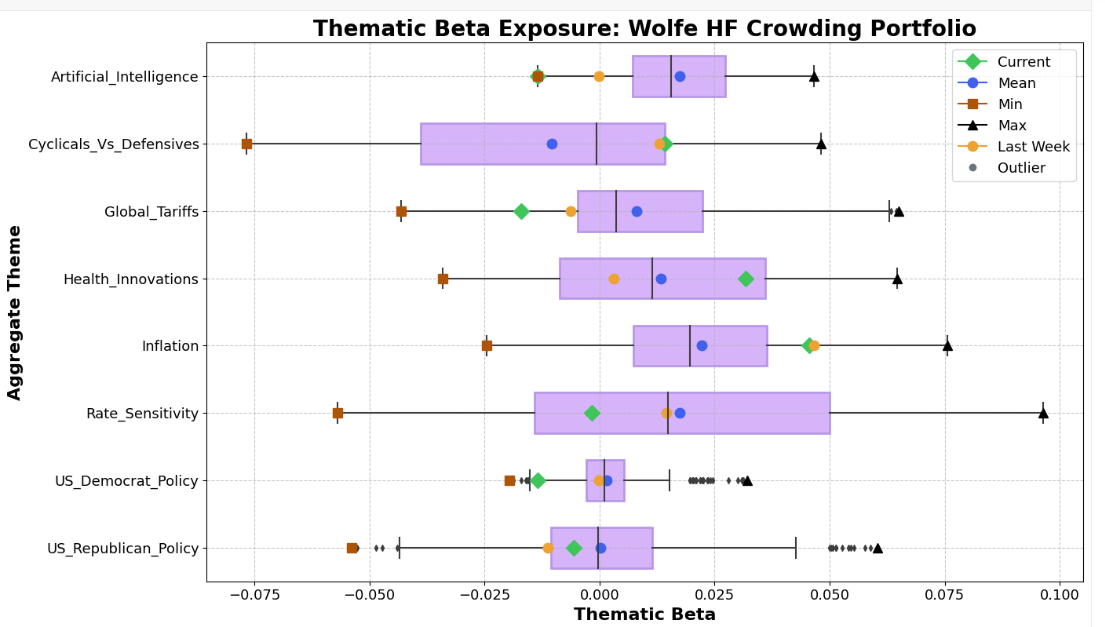

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Tariffs reintroduce geopolitical dispersion risk. While tariff beta has eased, markets are repricing higher geopolitical and trade-policy uncertainty following Trump’s Greenland-linked tariffs and rising EU retaliation risk. Expect headline-driven volatility and greater cross-asset and cross-sector dispersion, favoring selective positioning over broad risk exposure and penalizing trade-sensitive, export-heavy assets.

- Rates neutrality masks asymmetric duration risk. Rate-cut expectations have moderated, but a higher volatility regime persists. Sticky term premia, driven by fiscal concerns, Fed independence risks, and structurally weaker foreign demand for Treasuries, point to upward pressure on long-end yields. This backdrop argues for underweight duration, favor curve steepeners, and tilt toward rate-resilient equities.

- Health innovation offers idiosyncratic growth with defensive qualities. A pickup in IPO activity and sustained pharma-led M&A has revived sentiment across health innovation, supporting premium valuations. The theme provides alpha via deal optionality and pipeline catalysts, while also serving as a partial hedge in volatile macro environments due to low economic cyclicality.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- How should portfolios balance rising geopolitical and policy-driven volatility against selective risk opportunities? With tariffs, Fed independence concerns, and rate volatility driving dispersion, should allocations favor defensiveness and idiosyncratic alpha (e.g., Quality, Health Innovation), or is volatility creating entry points in cyclicals and Value?

- Does the combination of sticky term premia and weaker foreign demand for Treasuries require a structural rethink of duration exposure? As fiscal concerns, refinancing risks (especially in small caps), and geopolitical uncertainty pressure long-end yields, should investors reframe bonds from ballast to source of risk, and adjust equity factor tilts accordingly?

- Are recent leadership shifts signaling a regime change or a tactical rotation? With Value outperforming Growth, small caps showing fragile leadership, and Health Innovation benefiting from M&A and IPO momentum, is the market transitioning to a new factor regime—or are these moves best expressed through short-horizon, selective positioning?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses highlights a market leaning back into risk even as underlying fragilities persist. Institutions are selectively rotating toward cyclicals, and tentatively re-embracing AI—but each theme carries asymmetric risks tied to policy timing, late-cycle dynamics, and unproven profitability.

This week’s Lenses highlights a gradual return of risk appetite, with rate-sensitive trades, cyclicals, and even short-squeeze names showing renewed strength. Yet record highs in gold, flat performance in Technicals, and unresolved tariff risks underscore that this rotation remains tentative...

This week’s Lenses highlights mounting macro uncertainty as hedge funds unwind crowded trades and volatility picks up across inflation and rate-sensitive themes. Healthcare remains a rare bright spot, balancing defensive appeal with policy risk, while the rally narrows around a few megacap winners. With cyclicals struggling to stage a true comeback and investors cautious ahead of September’s Fed meeting, markets remain fragmented, demanding agility and selective conviction.