Markets Lean Risk-On Even as Policy Turns Cautious

Synopsis

Markets are navigating a delicate balance between resilient growth signals and renewed policy caution. Powell’s hawkish tone and sticky inflation expectations have tempered rate-cut optimism, yet institutional flows show investors rotating into cyclicals and maintaining exposure to growth and quality factors—betting that earnings strength can offset tighter financial conditions. Tariff developments and moderate breakevens underscore that inflation risks remain alive, leaving the Fed little room for error and investors increasingly reliant on selectivity rather than broad beta for returns.

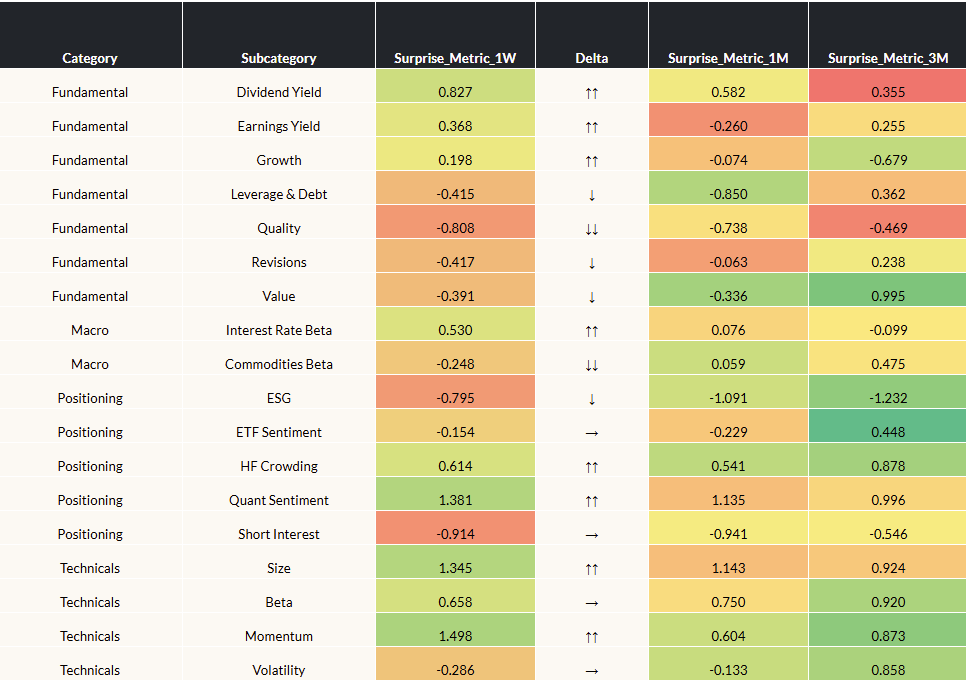

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 10/31/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Fed rhetoric resets easing expectations: Markets sold off as Chair Powell’s comments dampened hopes for a December rate cut, signaling that policy may stay tighter for longer. Despite the pullback, strong Q3 earnings breadth across the S&P 500 reinforces that economic resilience extends beyond large-cap tech.

- Cyclicals outperform amid mixed factor signals: Growth and Momentum factors surprised to the upside while Value and Quality lagged, underscoring a risk-on tone that persists even in a hawkish policy environment. Easing trade tensions with China may further stabilize inflation expectations and support cyclical exposure.

- Quant and crowding themes gain traction: Positioning factors such as Crowding and Quant Sentiment advanced sharply, reflecting continued institutional appetite for Growth and Quality tilts anchored in mega-cap AI and tech names—a concentration that remains a key driver of market performance.

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Cyclicals regain leadership: Institutional portfolios have rotated decisively from defense to offense, with cyclicals now showing positive thematic beta. Despite data uncertainty from the government shutdown, flows into growth-linked sectors suggest renewed conviction in the soft-landing narrative and appetite for risk assets.

- Markets reprice policy and inflation risk: Rate sensitivity has turned positive as investors adjust expectations for a shallower easing path amid Powell’s cautious tone and persistent fiscal concerns. Breakevens near 2.3–2.4% indicate markets see inflation moderating—but staying above target—keeping real yields elevated and duration trades delicate.

- Tariff tailwinds and policy friction: A rebound in tariff beta reflects optimism over a potential U.S.–China thaw, but with execution risk still high. New data from Bank of America showing tariffs adding roughly 30–50 bps to core inflation reinforce the view that trade policy remains an inflation wildcard—limiting the Fed’s room to ease and tempering enthusiasm for rate-sensitive equities.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

Is the rotation into cyclicals sustainable?

Institutional positioning has turned risk-on, but much of the move appears sentiment-driven rather than data-backed. If growth momentum falters or fiscal tensions reprice yields higher, cyclical leadership could prove short-lived.

How anchored are inflation expectations?

Breakevens near 2.3–2.4% signal moderate inflation ahead, yet tariff-related cost pressures and persistent fiscal deficits could keep expectations sticky. Investors may need to reassess whether real yields have fully priced the “higher for longer” regime.

Does policy risk now outweigh macro risk?

Between a cautious Fed, contested tariff authority, and widening deficits, policy uncertainty may be a greater volatility driver than economic data. Positioning discipline—especially in crowded growth and AI exposures—could define alpha generation through year-end.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses we explore markets advancing on genuine, broad-based strength, with earnings beats and technical breakouts supporting risk across sectors and styles. Within that upswing, capital is rotating toward exposures that benefit from growth without relying on falling rates—favoring Value, Cyclicals, Quality, and large-cap Momentum. The key shift isn’t a pullback from risk, but a higher bar for duration and capital intensity, leaving AI and rate-sensitive trades to earn their keep on fundamentals rather than narrative.

This week’s Lenses explores a market rewarding real-economy exposure and broadening leadership, supported by resilient consumption, benign inflation, and contained policy and trade risks. Suppressed volatility and unrewarded beta continue to favor Value, commodities, and selective cyclicals over momentum-heavy Growth. Until inflation or policy shocks reprice risk, returns are likely driven by breadth, factor selection, and real asset exposure rather than broad risk-on beta.

Markets are increasingly pricing a mid-to-late cycle environment where recession risk is deferred but growth remains uneven, supporting risk assets without requiring re-acceleration. Policy uncertainty—via Fed independence rhetoric and looming tariff rulings—has replaced macro data as the primary volatility driver, reinforcing higher-for-longer dynamics, curve steepening, and selective sector rotation. Across equities, leadership is narrowing as investors favor Value, cyclicals with pricing power, and AI names with visible cash flows, signaling a decisive shift from broad beta toward disciplined, fundamentals-driven positioning.