Late-Cycle Rotation Deepens: Value Holds Ground While Credit Risks Resurface

Synopsis

This week’s Lenses explores how late-cycle dynamics are reshaping market leadership and sentiment. Value continues to outperform as structurally higher inflation limits the Fed’s room to ease, while renewed credit stress—from Zions’ loan losses to high-profile bankruptcies—has investors questioning the depth of underlying fragility. Meanwhile, positioning unwinds and a tentative rotation back into cyclicals suggest that markets are still willing to test a soft-landing narrative, even as inflation data and policy noise threaten to blur that path.

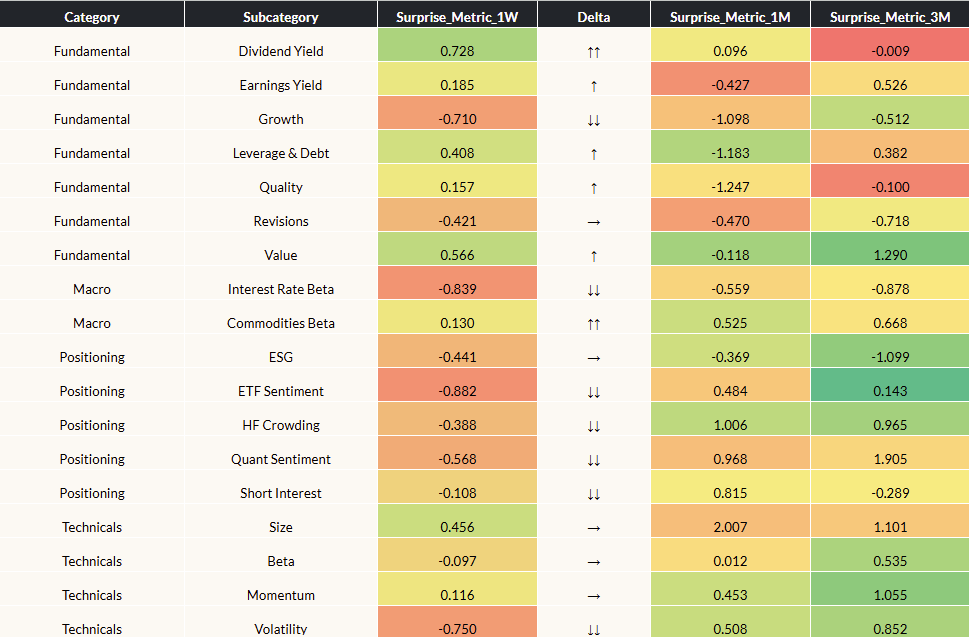

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 10/17/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Value leadership entrenches: The Value factor extended its lead over Growth — a hallmark of late-cycle regimes where inflation remains sticky and real activity slows. Structurally higher prices act as a floor under nominal earnings for asset-heavy sectors, while also limiting the Fed’s ability to ease, reinforcing Value’s advantage as real rates stay elevated and cash flows near term.

- Credit stress flashes amber: Zions National Bank’s charge-offs on bad commercial loans, combined with the bankruptcies of Tricolor Holdings and First Brands, stirred renewed anxiety over hidden credit risks across regional banks and private credit channels. The episode bolstered bearish narratives, sparking outflows from Growth and high-beta sectors as investors reassessed systemic fragility.

- Positioning unwinds accelerate: Sharp declines in hedge fund crowding, ETF sentiment, and quant momentum point to a broad rotation out of consensus risk-on trades. The VIX spike and subsequent drawdown suggest position de-risking rather than panic, but with a government shutdown pause and a wave of incoming data ahead, policy visibility may blur further, sustaining volatility into year-end.

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Cyclical-Defensive rotation normalizes: The sharp rebound in cyclicals brought the theme back to neutral after weeks of defensive bias, signaling a broad unwind in institutional positioning and a possible “buy-the-dip” rotation ahead of Q3 earnings. Whether this momentum turns into a sustained pro-cyclical move will depend on earnings breadth and macro durability, both of which remain uncertain amid slowing global data.

- Tariff trade fatigue sets in: Despite heavy headlines, the Tariff theme sank toward historical lows, implying that investors are fading policy-linked sectors expected to benefit from trade barriers. While tariff-driven inflation remains a latent risk to the disinflation narrative, markets appear conditioned to fade protectionist shocks—a pattern reinforced by expectations that policy noise often softens before material impact (“TACO” effect).

- Inflation risk back in focus: Inflation sensitivity turned lower last week, but all attention now shifts to Friday’s CPI print. With markets pricing an October cut as a near-certainty, even a mildly hot print could reignite rate-path uncertainty, complicating the easing narrative and testing the durability of the risk rebound.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

Is Value leadership durable—or just a function of rate fatigue? With structurally higher inflation limiting Fed flexibility, can Value’s outperformance persist once growth data begins to weaken, or will renewed easing expectations pull capital back toward duration-heavy Growth?

Are credit cracks isolated or systemic? Recent bankruptcies and regional bank losses have revived concern over hidden leverage in private credit and C&I lending. How much stress can the system absorb before liquidity tightens and funding markets reprice risk?

Can markets sustain risk-on momentum amid policy noise? The unwind in positioning and shift back toward cyclicals suggest investors are probing for a soft-landing trade—but with CPI risk, tariff uncertainty, and post-shutdown data volatility ahead, will sentiment hold or slip back into defensive mode?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses we explore markets advancing on genuine, broad-based strength, with earnings beats and technical breakouts supporting risk across sectors and styles. Within that upswing, capital is rotating toward exposures that benefit from growth without relying on falling rates—favoring Value, Cyclicals, Quality, and large-cap Momentum. The key shift isn’t a pullback from risk, but a higher bar for duration and capital intensity, leaving AI and rate-sensitive trades to earn their keep on fundamentals rather than narrative.

This week’s Lenses explores a market rewarding real-economy exposure and broadening leadership, supported by resilient consumption, benign inflation, and contained policy and trade risks. Suppressed volatility and unrewarded beta continue to favor Value, commodities, and selective cyclicals over momentum-heavy Growth. Until inflation or policy shocks reprice risk, returns are likely driven by breadth, factor selection, and real asset exposure rather than broad risk-on beta.

Markets are increasingly pricing a mid-to-late cycle environment where recession risk is deferred but growth remains uneven, supporting risk assets without requiring re-acceleration. Policy uncertainty—via Fed independence rhetoric and looming tariff rulings—has replaced macro data as the primary volatility driver, reinforcing higher-for-longer dynamics, curve steepening, and selective sector rotation. Across equities, leadership is narrowing as investors favor Value, cyclicals with pricing power, and AI names with visible cash flows, signaling a decisive shift from broad beta toward disciplined, fundamentals-driven positioning.