Markets Lean Into the Soft-Landing Trade as Fed Easing Beckons

Synopsis

This week’s Lenses explores how optimism around a dovish Fed and improving growth sentiment are reshaping market positioning. Softer inflation data has strengthened conviction in the easing cycle, fueling rotations into cyclicals, and high-beta exposures as investors price in a soft landing. Yet beneath the surface, the coexistence of risk-on positioning and renewed inflation hedging signals a market torn between confidence in policy support and anxiety over its durability—an uneasy equilibrium that could break quickly if growth or policy credibility wavers.

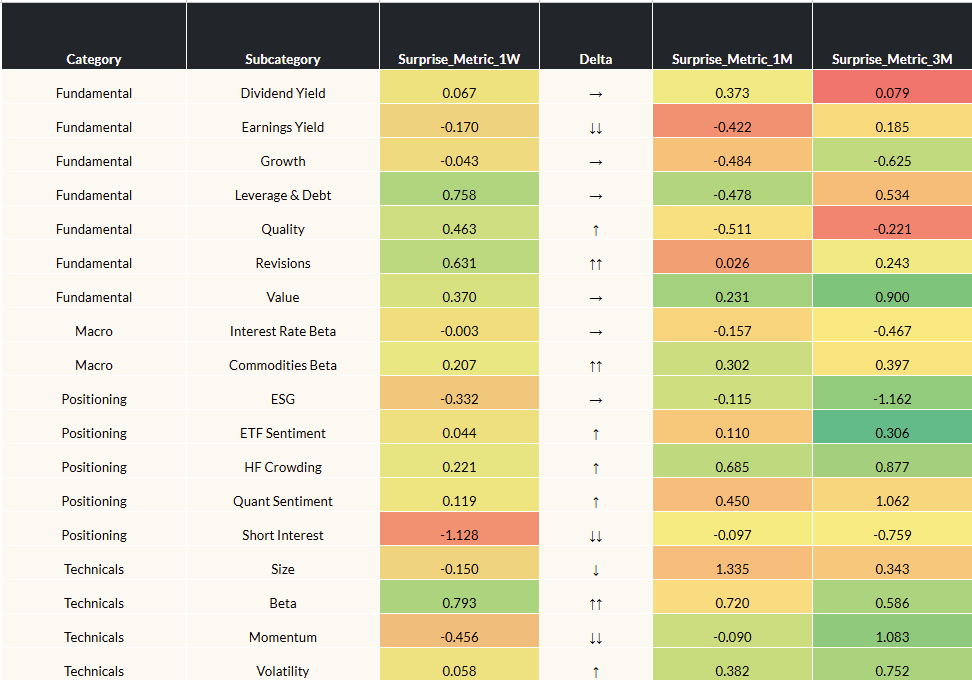

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 10/24/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Softer inflation print cements dovish expectations:

Markets took comfort in a cooler inflation release, effectively locking in expectations for a rate cut at Wednesday’s FOMC meeting. The print reinforces the narrative that disinflation remains intact, giving the Fed cover to ease even as growth data shows cracks. With labor market softness and slowing demand outweighing inflation risks, investors are extending duration and leaning into duration-sensitive assets—while maintaining optionality in case policy relief proves insufficient to reaccelerate growth. - Value strength endures, but breadth narrows:

Factor performance was largely stable, with Value maintaining leadership over Growth and Quality modestly improving. The interplay between easing policy and resilient regional PMIs suggests cyclicals could remain supported near-term, but fragility beneath the surface—ranging from excess leverage to stalling job gains and potential AI-investment fatigue—raises questions about the durability of the rotation. The soft-landing thesis looks increasingly priced in, leaving little cushion if data weakens further. - Positioning signals tactical risk-on beneath defensive shift:

A steep drop in Short Interest, coupled with higher Beta and Size factor performance, points to aggressive short covering and renewed risk appetite. Yet flows into Healthcare and Utilities imply investors are not abandoning defense altogether—rather, they’re recalibrating toward yield-and-quality plays that can benefit from falling long rates and slower nominal growth. This mix of speculative repositioning and defensive preference reflects an uneasy balance between optimism on policy support and skepticism about its real-economy traction.

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Cyclicals vs. defensives march higher into FOMC:

The cyclical-defensive spread continued to widen as investors leaned into risk ahead of the Fed’s meeting, where another cut is fully priced. The key watchpoint isn’t the cut itself but the tone—if Powell leans dovish and signals an extended easing path, it could validate the risk-on rotation and reinforce positioning in growth-sensitive equities. Conversely, any hint of hesitation risks unwinding the rally as markets test the Fed’s confidence in the soft-landing narrative. - Inflation theme re-awakens as possible tail risk hedge:

Inflation beta rose sharply, suggesting institutions are rebuilding exposure to inflation-linked and real-asset plays even after a benign CPI print. The move likely reflects possible unease about policy lag effects and the possibility of upside inflation surprises once growth stabilizes. Positioning into commodity sensitive sectors may serve dual purpose—participation in a cyclical rebound while maintaining a tail hedge against renewed price pressures. - Rate sensitivity stabilizes as yield curve dynamics shift:

Rate Sensitivity climbed toward neutral as the 10-year yield rebounded above 4%, driven by improved growth sentiment and fading safe-haven demand. Optimism around U.S.–China trade and a higher term premium are steepening the curve, creating scope for relative-value trades such as steepeners and curve-caps. With front-end yields anchored by policy easing and long-end rates drifting higher on issuance and growth optimism, duration positioning may remain a key lever for macro portfolios.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

Has the easing cycle already been priced in?

With a Fed cut fully expected and dovish rhetoric anticipated, markets may have already front-loaded much of the policy optimism. The key risk is whether the easing path still carries incremental stimulus value—or whether markets have prematurely priced a soft landing that leaves limited upside for risk assets.

Inflation risk: cyclical hedge or structural threat?

Institutions appear to be adding inflation-sensitive exposures even as headline prints cool. Is this simply tactical positioning for a cyclical upswing, or recognition that structural drivers—deglobalization, fiscal expansion, and wage stickiness—could reignite price pressures once growth stabilizes?

Positioning under the surface: conviction or complacency?

The rise in Beta, Size, and cyclical exposure alongside flows into defensives suggests a market straddling both risk-on optimism and macro caution. Are investors expressing genuine conviction in a policy-backed recovery—or merely crowding into a narrow set of trades that could unwind quickly if growth data disappoints?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses we explore markets advancing on genuine, broad-based strength, with earnings beats and technical breakouts supporting risk across sectors and styles. Within that upswing, capital is rotating toward exposures that benefit from growth without relying on falling rates—favoring Value, Cyclicals, Quality, and large-cap Momentum. The key shift isn’t a pullback from risk, but a higher bar for duration and capital intensity, leaving AI and rate-sensitive trades to earn their keep on fundamentals rather than narrative.

This week’s Lenses explores a market rewarding real-economy exposure and broadening leadership, supported by resilient consumption, benign inflation, and contained policy and trade risks. Suppressed volatility and unrewarded beta continue to favor Value, commodities, and selective cyclicals over momentum-heavy Growth. Until inflation or policy shocks reprice risk, returns are likely driven by breadth, factor selection, and real asset exposure rather than broad risk-on beta.

Markets are increasingly pricing a mid-to-late cycle environment where recession risk is deferred but growth remains uneven, supporting risk assets without requiring re-acceleration. Policy uncertainty—via Fed independence rhetoric and looming tariff rulings—has replaced macro data as the primary volatility driver, reinforcing higher-for-longer dynamics, curve steepening, and selective sector rotation. Across equities, leadership is narrowing as investors favor Value, cyclicals with pricing power, and AI names with visible cash flows, signaling a decisive shift from broad beta toward disciplined, fundamentals-driven positioning.