Risk-On, But Not Risk-Free

Synopsis

This week’s Lenses highlights a market cautiously embracing re-risking while quietly testing the durability of its own narrative. Beneath the surface, investors are rotating away from crowded growth trades and toward real-economy and structural themes, even as policy ambiguity, tariff noise, and looming data releases limit conviction. The common thread: markets want to lean risk-on, but the path forward hinges on whether fundamentals can validate early signs of a leadership shift.

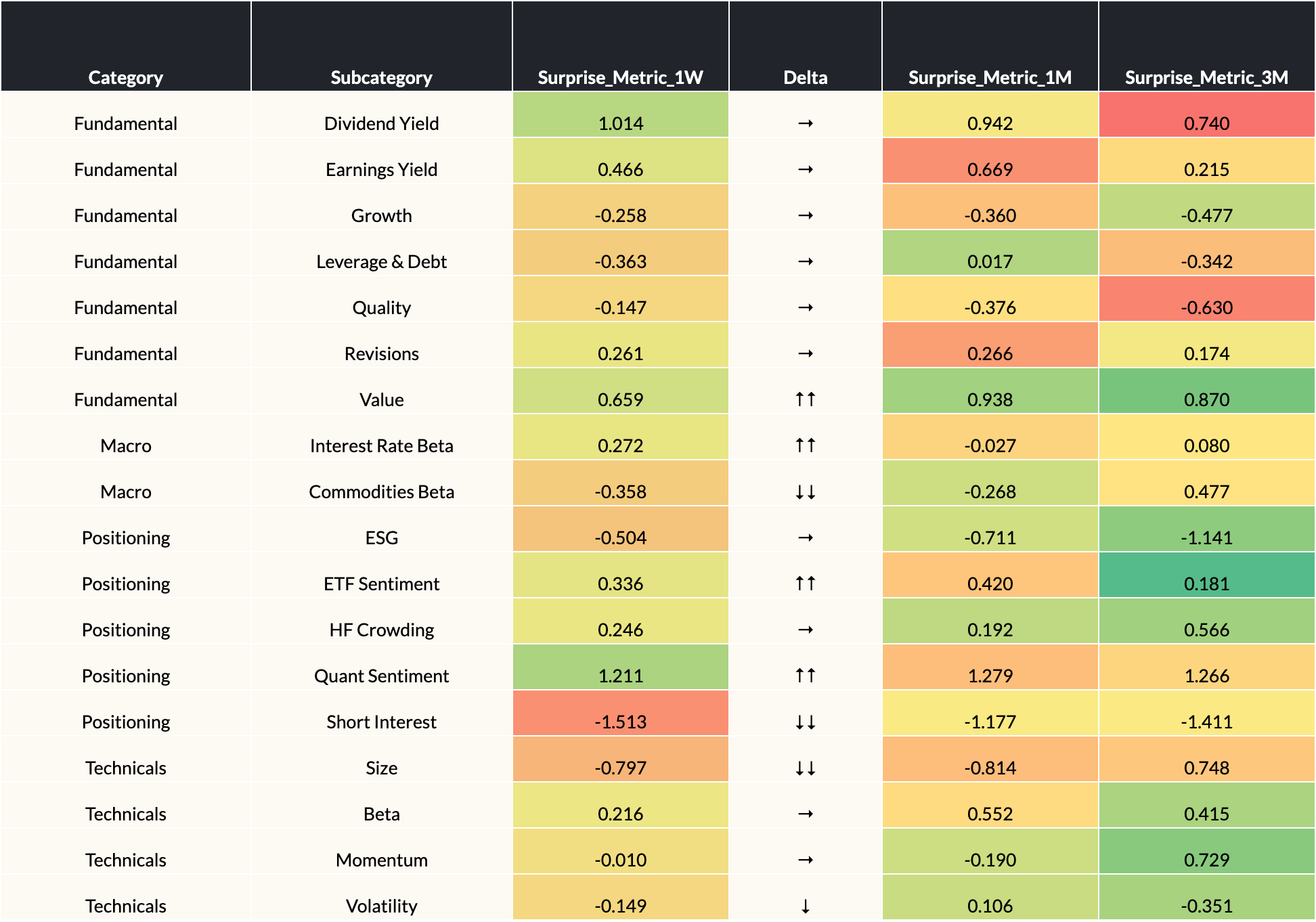

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 12/12/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Markets are leaning into a re-risking regime after the well-telegraphed 25 bp cut, but policy uncertainty tempers the upside. Lower rates boosted small caps, Value, and rate-sensitive sectors like Financials, while the surprise reinstatement of Treasury buying added fresh liquidity. But the Fed’s more restrictive tone on 2026 limits how far investors can extrapolate easing, keeping medium-term positioning cautious.

- Tech fragility is re-emerging as crowded leadership confronts fundamental disappointments. Oracle and Broadcom’s misses redirected attention from long-dated AI growth to near-term return discipline, pressuring Growth and Momentum factors and extending Tech’s underperformance. Capital is rotating toward real-economy cyclicals—Industrials, Materials, and other less-crowded segments—as investors rebalance risk exposure.

- This week’s labor and inflation data will determine whether re-risking has legs or stalls out. CPI is expected to hold near 3% and labor softness remains anchored by structural forces, even as the Fed looks through tariff effects and anticipates disinflation in 2026. A benign data path supports continued beta exposure, while any upside surprises could quickly unwind the early-cycle narrative forming in markets.

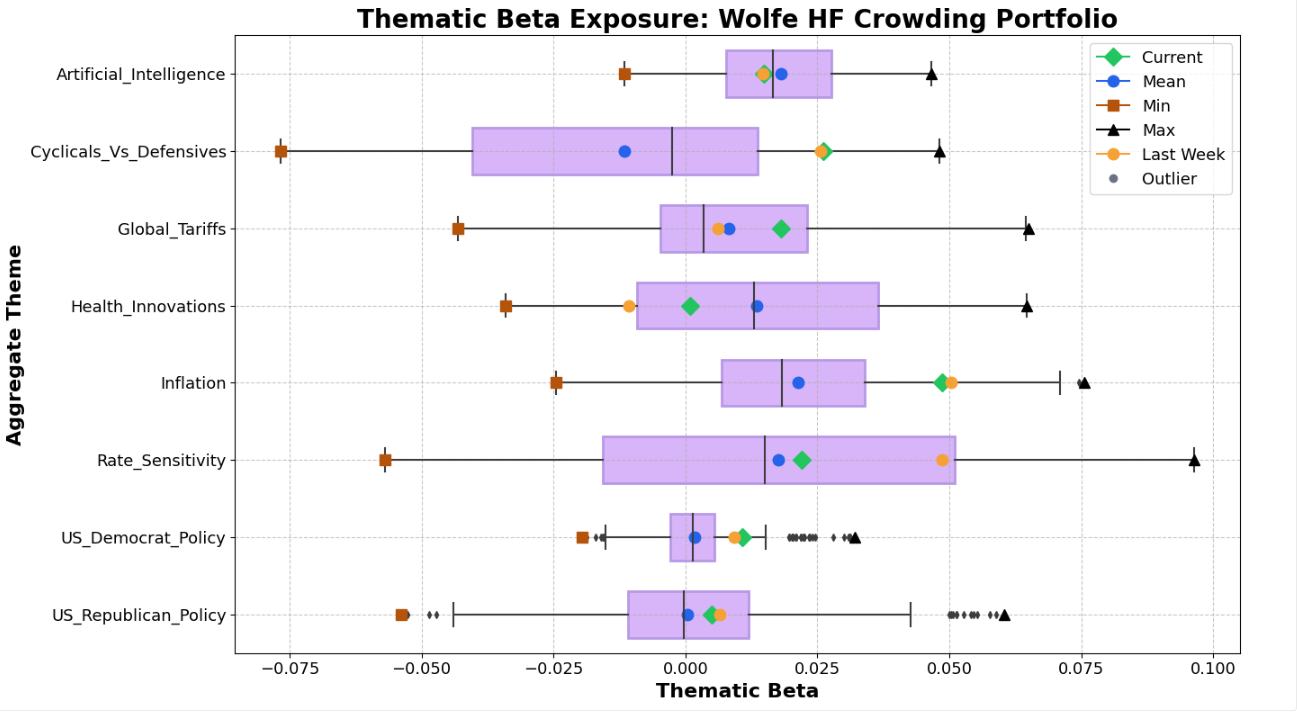

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Thematic activity was broadly muted into the holiday slowdown, but tariff-linked signals continue to warrant monitoring. U.S.–UK tech cooperation pauses and potential tariff reductions on Swiss imports nudged the Tariff theme higher, though the bigger swing factor remains the Prices Paid index—where any re-acceleration would challenge the market’s soft-landing consensus. For now, we still view cost-push inflation risk as low probability but high sensitivity for positioning.

- Health Innovation regained relevance as investors balanced near-term rotation with selective structural tailwinds. Sector underperformance earlier in the week points to profit-taking, yet ongoing IPO activity and strategic M&A in diagnostics and services reinforce a constructive long-term thesis. This keeps the theme viable as a diversifier, especially amid factor volatility and fading Tech leadership.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- How durable is the re-risking impulse if upcoming labor and inflation data fail to confirm the early-cycle narrative? Markets embraced the rate cut and liquidity boost, but the Fed’s 2026 tone and lingering cost-push risks (via Prices Paid) leave little margin for upside surprises.

- Is the rotation away from crowded Tech into real-economy cyclicals the start of a broader leadership shift—or just a positioning clean-up after earnings shocks? Oracle and Broadcom exposed the fragility of AI-linked growth expectations, raising questions about where sustainable return on capital will re-emerge.

- Can Health Innovation reassert itself as a structural compounder even as broader Healthcare suffers rotations and margin concerns? IPO momentum and M&A activity contrast with sector underperformance, making it a timely case study in how investors distinguish long-term thematic value from near-term defensiveness.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

In this week’s Lenses we explore markets advancing on genuine, broad-based strength, with earnings beats and technical breakouts supporting risk across sectors and styles. Within that upswing, capital is rotating toward exposures that benefit from growth without relying on falling rates—favoring Value, Cyclicals, Quality, and large-cap Momentum. The key shift isn’t a pullback from risk, but a higher bar for duration and capital intensity, leaving AI and rate-sensitive trades to earn their keep on fundamentals rather than narrative.

This week’s Lenses explores a market rewarding real-economy exposure and broadening leadership, supported by resilient consumption, benign inflation, and contained policy and trade risks. Suppressed volatility and unrewarded beta continue to favor Value, commodities, and selective cyclicals over momentum-heavy Growth. Until inflation or policy shocks reprice risk, returns are likely driven by breadth, factor selection, and real asset exposure rather than broad risk-on beta.

Markets are increasingly pricing a mid-to-late cycle environment where recession risk is deferred but growth remains uneven, supporting risk assets without requiring re-acceleration. Policy uncertainty—via Fed independence rhetoric and looming tariff rulings—has replaced macro data as the primary volatility driver, reinforcing higher-for-longer dynamics, curve steepening, and selective sector rotation. Across equities, leadership is narrowing as investors favor Value, cyclicals with pricing power, and AI names with visible cash flows, signaling a decisive shift from broad beta toward disciplined, fundamentals-driven positioning.