Reflation Rumbles, Policy Fades as Markets Pivot Toward Resilience

Synopsis

This week’s Lenses spotlights renewed rotation as inflation expectations rise, rate-sensitive sectors rebound, and leadership briefly shifts back to megacap tech. Meanwhile, policy-driven trades—like Republican beta and tariff beneficiaries—continue to fade, reflecting a broader pivot toward defensives and fundamentals. With Fed signals and earnings in play, investors face a market defined by fragility, crowding, and the need for tactical flexibility.

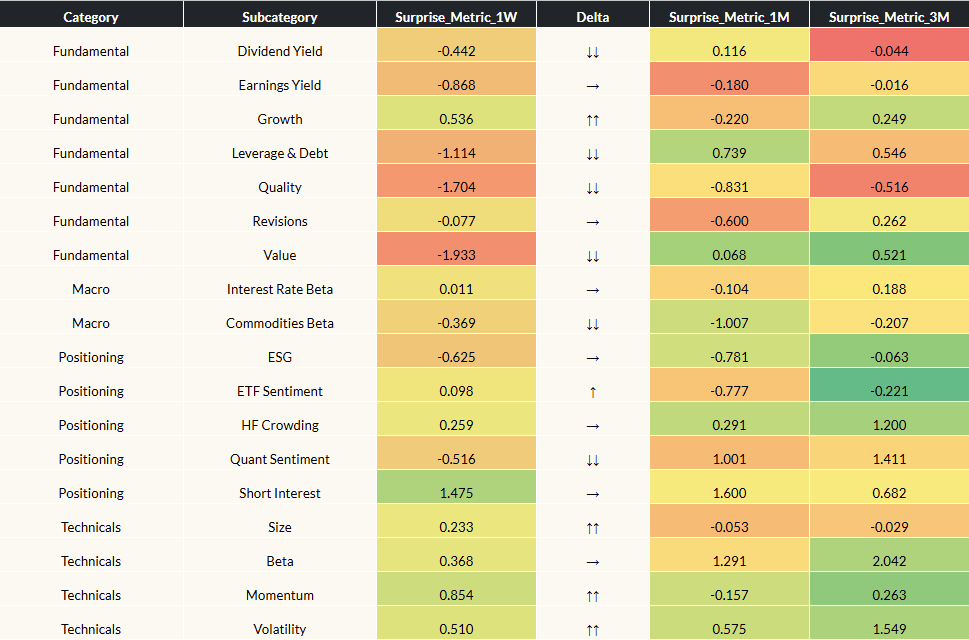

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 7/18/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previousweek and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Growth snaps back, Value stumbles - Growth stocks rebounded sharply last week, led by megacap tech, while Value lagged as long-term yields ticked higher before easing. Despite the move, medium-term trends still favor Value, supported by rising risk appetite and recent weakness in Quality. Investors should watch closely for changes in Fed policy guidance, 10Y yields, and key Q2 tech earnings —as these will shape where the rotation goes next.

- Hedge funds rotate defensively - Quant sentiment softened while Short Interest, ETF Sentiment, and HF Crowding all stayed in positive territory—signaling that broad rotations and re-positioning are still occurring. Hedge funds specifically have been increasing shorts in financials and consumer discretionary—sectors that the broader market has favored. This divergence is worth tracking for signs of stress or positioning extremes.

- Momentum and Size bounce, but stay lukewarm. Last week’s rally in big tech lifted Momentum and Size factors, but underlying trends remain shaky. Investors should be cautious about chasing these short-term gains until there’s clearer confirmation that past-leadership is returning sustainably.

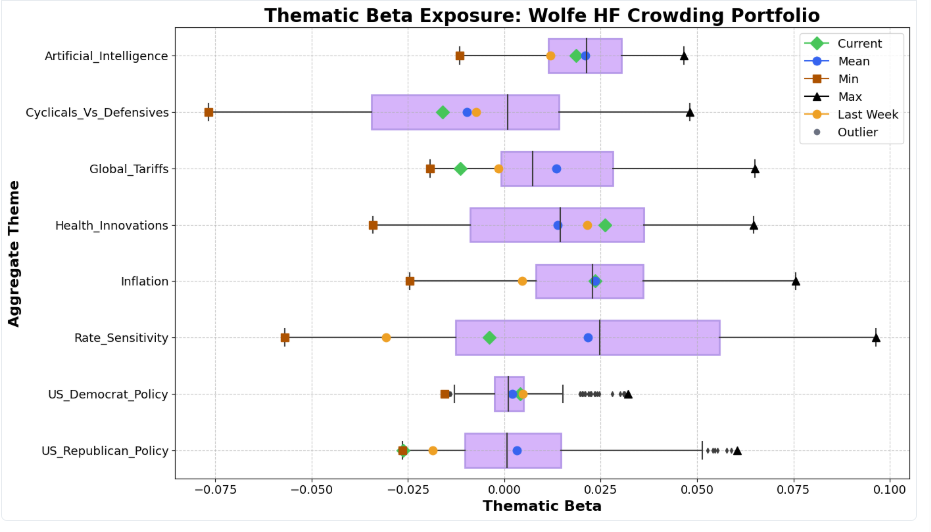

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Rate sensitivity and inflation trades are back in play. With 5-year breakevens settling at 2.5%, inflation concerns are resurfacing, while dovish commentary from some Fed officials pushed yields lower. This sets the stage for a summer shaped by reflation anxiety—investors should position carefully around sectors sensitive to both rate direction and pricing power.

- Republican policy beta sinks to new lows. Cyclical sectors like Financials and Energy, once favored under GOP-aligned policy themes, are now under pressure as hedge funds take short positions or rotate out of these sectors into defensives. This shift signals fading conviction in cyclical driven narratives—and growing interest in stability of chasing upside.

- Tariff exposure fades as a market driver. The tariff theme continues to lose momentum, with most earnings impacts likely priced in. For investors, residual alpha is now tied more to inflation spillovers than to direct trade policy—making the theme less relevant for tactical positioning.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

- Are we positioned for the return of inflation and rate sensitivity? With inflation expectations rising and Treasury yields easing on dovish Fed signals, rate-sensitive sectors are back in focus. Are we aligned with this shift—balancing exposure to real estate, utilities, and yield plays without overextending?

- Are we moving on from yesterday’s macro winners? Republican policy-linked sectors and tariff trades are fading from relevance. Are we reallocating toward more resilient areas—defensives, quality, and secular growth—as the market shifts?

- Are we ready for fragile leadership and fast rotations? Momentum and Size bounced on tech strength and short-covering, but underlying trends remain shaky. Are we set to capture tactical upside without getting caught in crowded or fading trades?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This Week’s Lenses explores how markets are shifting from speculative enthusiasm to selective resilience. Healthcare Innovation’s ascent from laggard to leader highlights investor appetite for quality growth amid a “higher for longer” rate backdrop, while softening political policy momentum underscores rising policy and macro uncertainty. Together, they reveal a market recalibrating toward fundamentals, balance-sheet strength, and defensiveness over narrative-driven risk.

This week’s Lenses spotlights a market leaning defensive beneath the surface, with institutions shunning cyclicals even as retail exuberance lingers.

This week’s Lenses spotlights rapid market rotation as investors react to new tariffs, shifting rate bets, and policy uncertainty. Hedge fund flows, sector leadership, and crowded trades are all in flux, highlighting the need for agile positioning amid ongoing headline risk.