Defensives Take the Wheel as Retail Chases Risk and Tariff Fears Morph Into Inflation Threats

Synopsis

This week’s Lenses spotlights a market leaning defensive beneath the surface, with institutions shunning cyclicals even as retail exuberance lingers. Healthcare innovation stands out as a rare area offering both resilience and selective upside, while tariff risks have slipped from focus—though their inflationary effects may prove stickier than growth impacts. With policy moves and seasonal volatility looming, investors face a backdrop where caution, rather than conviction, is quietly steering positioning.

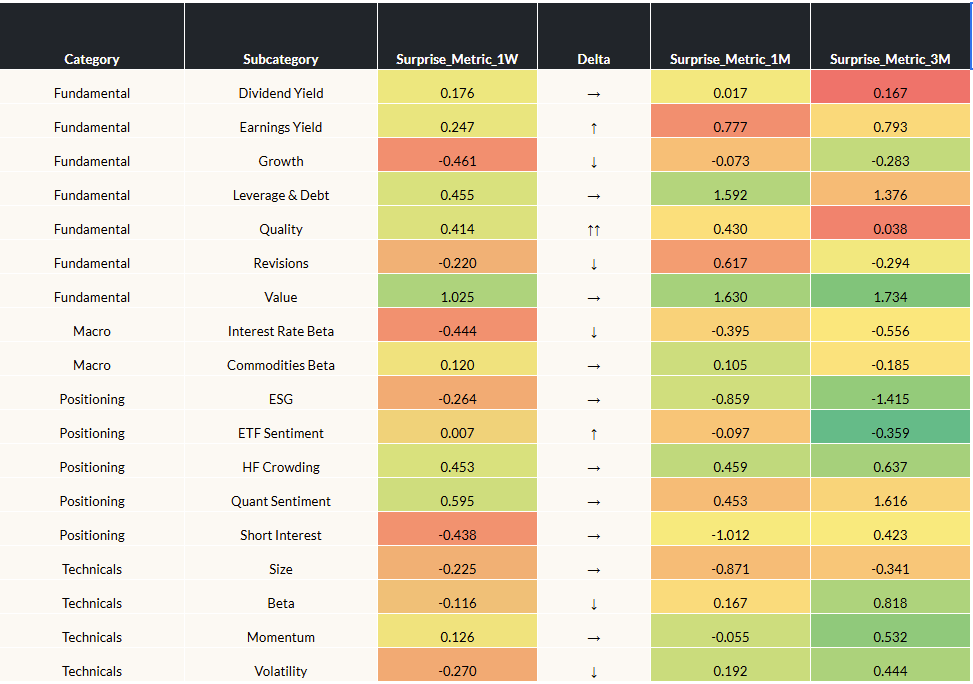

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 9/5/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Defensives staged a rebound as Earnings Yield and Quality recovered from last week’s selloff. The weak NFP print locked in expectations for a September cut, but also heightened concern the Fed is lagging the cycle. If labor data keeps deteriorating or the cut underwhelms, investors are likely to rotate more aggressively back into defensive factors.

- Rate-sensitive positioning remains fragile, with Interest Rate Beta still negative and Commodities Beta barely holding positive. Institutions are broadly leaning into easing, but a hot inflation surprise or renewed oil price pressure could inject volatility into rate- and commodity-linked sectors.

- Cyclicals lost momentum, with Beta and Vol selling off as labor market jitters took hold. Their outlook depends on cuts being strong enough to revive hiring and growth—but the risk is twofold: a Fed that’s already behind the curve, or inflation reaccelerating and forcing a pause, both scenarios reinforcing stagflation fears.

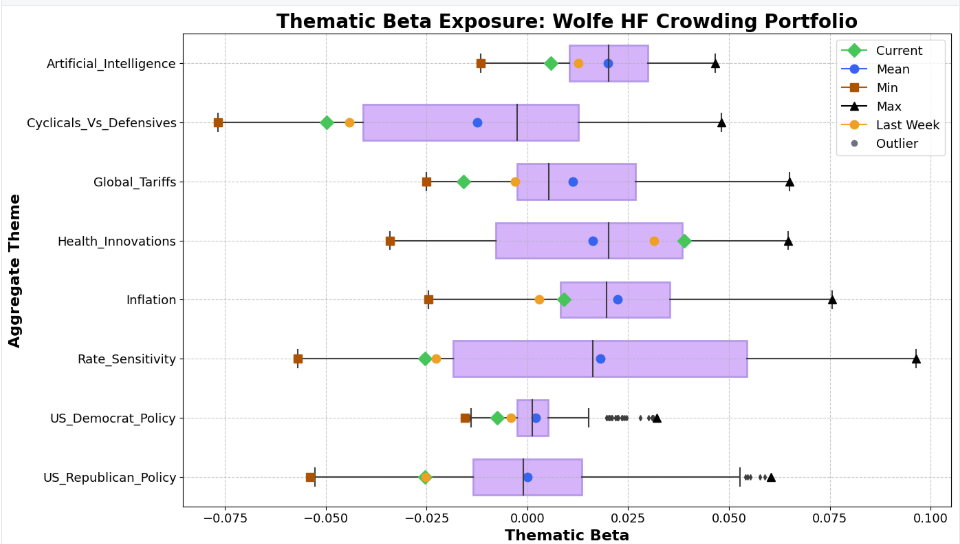

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Cyclicals vs. Defensives remain under pressure, highlighting the divergence between retail optimism and institutional caution. Institutions continue to favor safety even as retail chases risk, and the coming weeks—shaped by policy signals and seasonal volatility—will determine if defensive positioning hardens or finally gives way to risk-on rotation.

- Healthcare innovation is still climbing, with bright spots like GEHC outperforming even as the broader sector shows cracks from slowing employment growth. The space remains a defensive anchor, but its mix of resilience and selective upside makes it one of the few areas offering both protection and tactical opportunity.

- Tariff fears are fading from center stage, as institutional portfolios have largely moved past them. Market reactions are now brief bursts of volatility around announcements followed by quick stabilization, but the real lingering risk lies in tariffs fueling sticky inflation rather than choking near-term growth.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

Are defensives signaling deeper cracks beneath retail exuberance? With institutions leaning defensive even as retail chases cyclicals, will upcoming policy signals and seasonal volatility force a convergence—or deepen the divide between cautious and risk-seeking flows?

Can Healthcare balance its dual role as defense and growth? With sector-wide resilience masking slowing employment and innovation leaders like GEHC outperforming, does Healthcare remain a safe haven—or is it evolving into a tactical growth play with selective upside?

Are tariff risks truly behind us—or just morphing into inflation pressure? While headline tariff news is fading, the real impact may be through sticky inflation rather than growth drag. Are investors too quick to dismiss this risk in a market already leaning heavily on policy support?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This Week’s Lenses explores how markets are shifting from speculative enthusiasm to selective resilience. Healthcare Innovation’s ascent from laggard to leader highlights investor appetite for quality growth amid a “higher for longer” rate backdrop, while softening political policy momentum underscores rising policy and macro uncertainty. Together, they reveal a market recalibrating toward fundamentals, balance-sheet strength, and defensiveness over narrative-driven risk.

This week’s Lenses spotlights renewed rotation as inflation expectations rise, rate-sensitive sectors rebound, and leadership briefly shifts back to megacap tech. Meanwhile, policy-driven trades—like Republican beta and tariff beneficiaries—continue to fade, reflecting a broader pivot toward defensives and fundamentals. With Fed signals and earnings in play, investors face a market defined by fragility, crowding, and the need for tactical flexibility.

This week’s Lenses spotlights rapid market rotation as investors react to new tariffs, shifting rate bets, and policy uncertainty. Hedge fund flows, sector leadership, and crowded trades are all in flux, highlighting the need for agile positioning amid ongoing headline risk.