Markets pivot fast as investors chase new themes and sidestep old risks

Synopsis

This week’s Lenses spotlights rapid market rotation as investors react to new tariffs, shifting rate bets, and policy uncertainty. Hedge fund flows, sector leadership, and crowded trades are all in flux, highlighting the need for agile positioning amid ongoing headline risk.

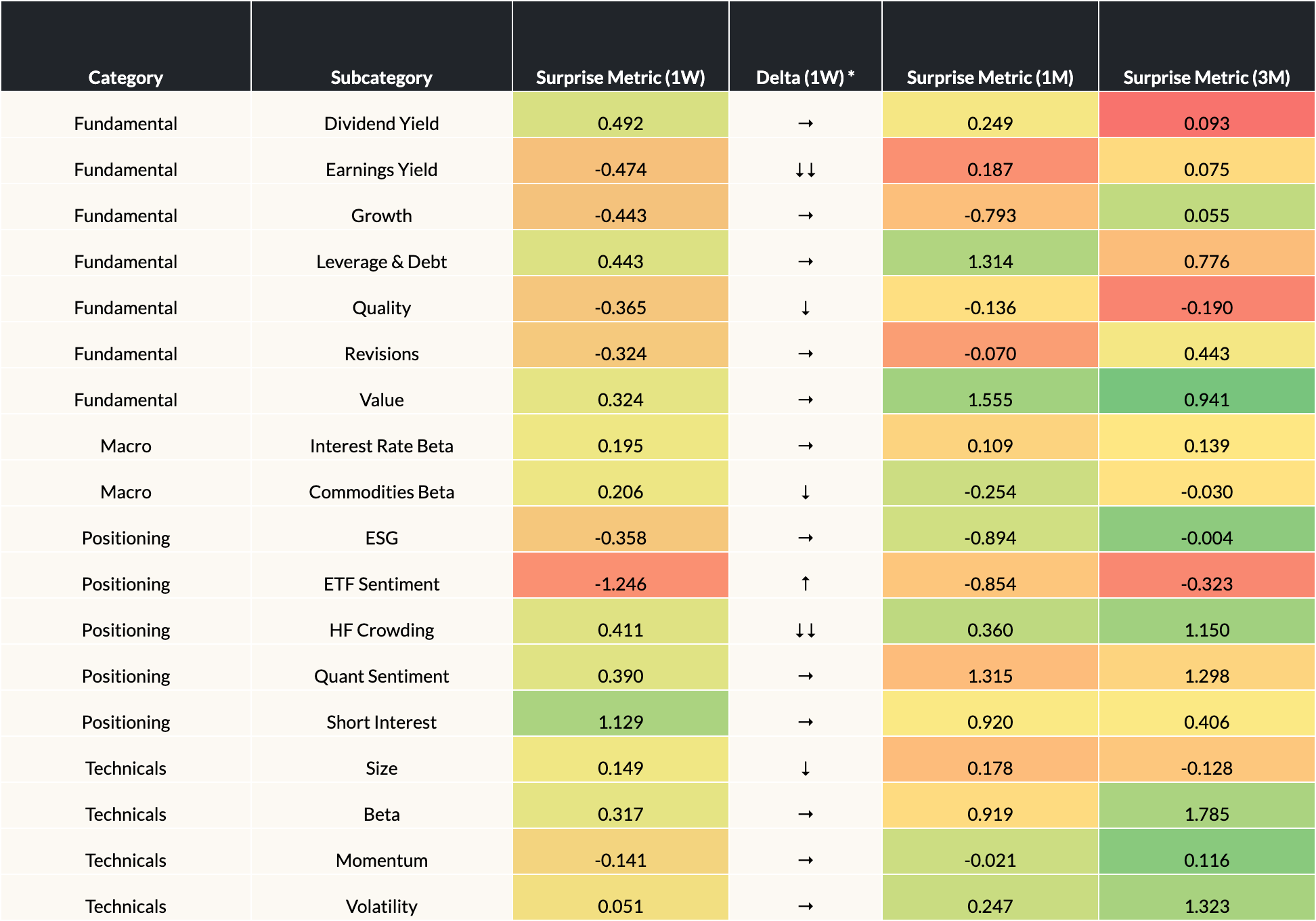

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 7/11/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previousweek and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Defensives may be losing their edge: Quality and Earnings Yield both softened this week, extending a trend of underperformance over 1M and 3M. Overvalued Quality names appear to be losing favor as risk appetite picks back up, while Q2 uncertainty seems to be weighing on low P/E stocks. Both factors could see a retracement if market conditions worsen later this year.

- Commodities starting to ascend: Commodities Beta factors is trending higher likely supported by renewed rate easing hopes, oil price headwinds, and continued de-dollarizing by foreign investors. Metals and Energy are likely drawing attention, as traders seek out assets most sensitive to policy pivots, inflation and further dollar declines.

- Crowded trades could be unwinding: ETF sentiment saw a modest uptick this week, but the longer-term trend remains lower, pointing to a larger rotation out of past winners. With Hedge Fund Crowding and Quant Sentiment also reversing, the risk of a disorderly unwind—and increased volatility—remains if the pace of selling picks up.

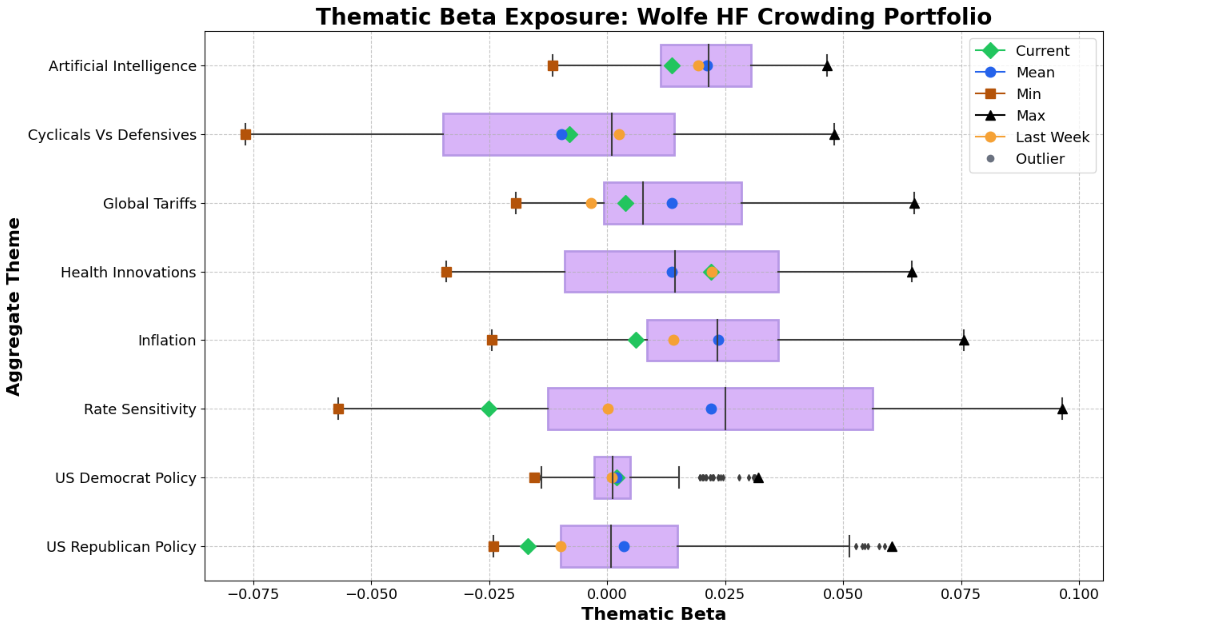

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024. How to read this graph

Highlights

- Tariff headlines nudge thematic risk higher: Tariff linked thematic beta ticked up this week as new tariff announcements reignited trade war concerns. However, the “TACO” (Trump Always Chickens Out) trade has softened the blow, with markets increasingly discounting tariff threats as political noise. For investors, this means tariff-sensitive sectors may remain volatile, but the actual impact could be muted unless policy rhetoric turns into real action.

- Cyclicals and Defensives retreat: Both cyclical and defensive stocks moved lower, signaling a reversal in hedge fund flows just as earnings season kicks off. With Trump’s tariffs set to hit corporate margins and reflect in economic outlooks this quarter, investor positioning could shift quickly. Expect heightened sector rotation and sharp swings depending on whether earnings results confirm or challenge market fears.

- Rate sensitivity beta turns sharply negative: Hedge funds have shifted to contrarian stances on rates, likely reacting to speculation about new Fed leadership and growing policy uncertainty. For investors, this pivot warns of potential surprises in traditional rate-sensitive plays—such as banks, real estate, and utilities—as shifting expectations could drive unexpected volatility across these sectors.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- Are we prepared for rapid sector rotations and shifting market leadership?

With hedge funds and ETFs quickly reversing flows, are we nimble enough to capture upside in favored sectors while protecting against sharp rotations and earnings-driven surprises—especially in areas exposed to tariffs and policy shifts? - How are we managing risk and opportunity as rate expectations and Fed policy remain in flux?

With rate-sensitive assets facing fresh volatility amid speculation over new Fed leadership and shifting rate bets, do we have the right balance of exposure in banks, real estate, and utilities to benefit from sudden market moves while limiting downside from unexpected policy shifts? - Do we have the flexibility to capitalize on policy and macro uncertainty without overreacting to headlines?

As tariff risks, political noise, and macro uncertainty continue to drive market sentiment, is our portfolio positioned to stay resilient—capturing opportunities in commodities, thematic trades, and policy beneficiaries, while not getting caught offside by transient news and crowd unwinds?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This Week’s Lenses explores how markets are shifting from speculative enthusiasm to selective resilience. Healthcare Innovation’s ascent from laggard to leader highlights investor appetite for quality growth amid a “higher for longer” rate backdrop, while softening political policy momentum underscores rising policy and macro uncertainty. Together, they reveal a market recalibrating toward fundamentals, balance-sheet strength, and defensiveness over narrative-driven risk.

This week’s Lenses spotlights a market leaning defensive beneath the surface, with institutions shunning cyclicals even as retail exuberance lingers.

This week’s Lenses spotlights renewed rotation as inflation expectations rise, rate-sensitive sectors rebound, and leadership briefly shifts back to megacap tech. Meanwhile, policy-driven trades—like Republican beta and tariff beneficiaries—continue to fade, reflecting a broader pivot toward defensives and fundamentals. With Fed signals and earnings in play, investors face a market defined by fragility, crowding, and the need for tactical flexibility.