Geopolitics High, Inflation Contained, Risks Asymmetric

Synopsis

Markets are entering 2026 with elevated geopolitical risk but sustained risk-taking, supported by liquidity, policy accommodation, and still-contained inflation expectations. Leadership remains conditional: cyclicals benefit in a soft-landing scenario, while growth could reassert if labor data weakens and policy easing accelerates. At the same time, the market’s heavy reliance on AI-driven upside introduces a new fragility, where any leverage unwind could quickly shift sentiment to risk-off.

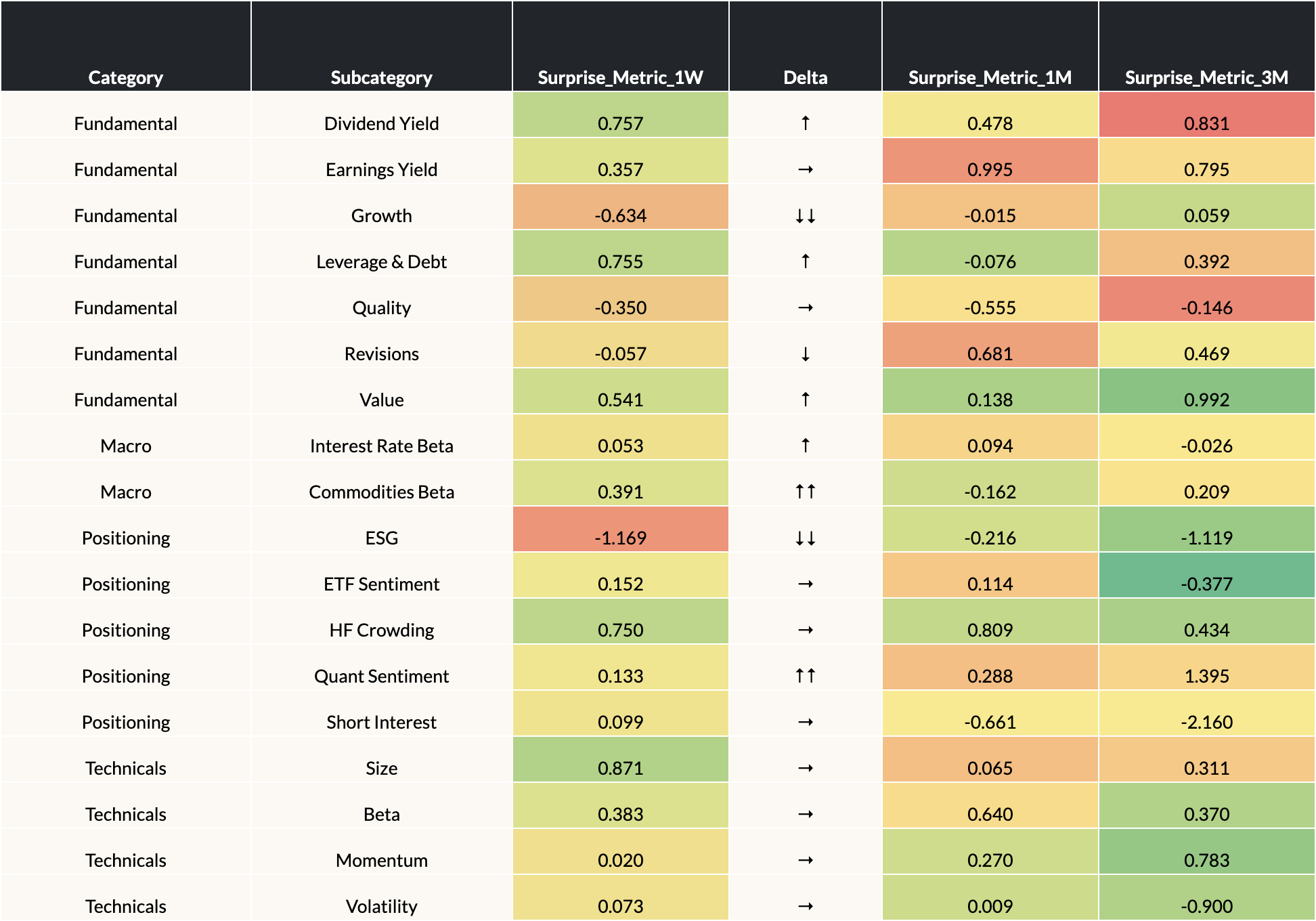

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 1/6/2026

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Risk premia rising, but risk appetite intact. 2026 is starting with elevated geopolitical uncertainty, yet investors continue to add risk. Tech sentiment has remained resilient on buy-the-dip behavior, while energy and commodities rallied on Venezuela-related headlines—though without evidence of imminent supply disruption, the move looks more sentiment- and beta-driven than fundamentally durable.

- Positioning and technicals remain a mild tailwind, not a catalyst. Most technical indicators were little changed on the week, but quant sentiment saw the largest positive inflection, even if it remains subdued versus three months ago. This suggests reduced downside pressure rather than a strong momentum signal, leaving markets sensitive to macro confirmation.

- Policy path is narrowing, shifting focus to labor data and growth optionality. The Fed’s year-end rate cut was well telegraphed, but a divided FOMC and market pricing for ~60bps of further easing cap near-term dovish expectations. A meaningful labor market slowdown—while not the base case—would force more extreme policy action and reopen the easing narrative. Which coupled alongside OBBB tax incentives could re-ignite the Growth factor after late-2025 underperformance.

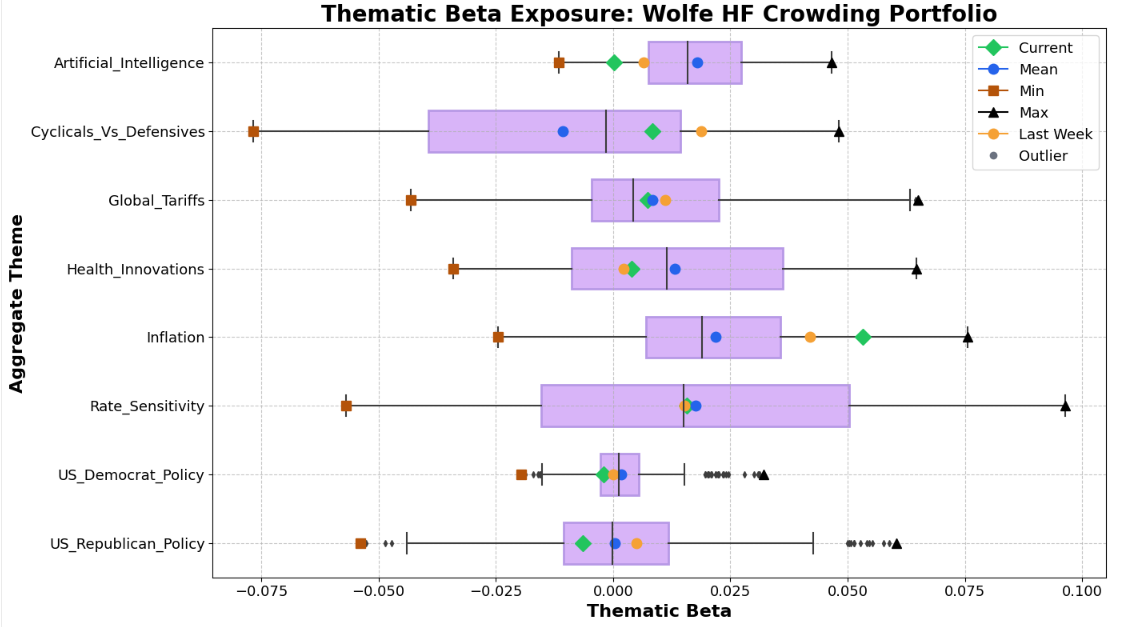

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Cyclical tilt remains supported despite near-term consolidation. Cyclical vs. Defensive theme retreated from last week but remains higher than its 2025 average. An accommodative policy backdrop, incremental liquidity from Treasury purchases, and OBBB tax cuts should continue to favor cyclicals in a soft-landing scenario. A sharper-than-expected labor market downturn would likely shift the market from cyclical optimism toward policy-driven, duration- and growth-led outcomes instead.

- Inflation risks remain contained, with upside skewed to geopolitics rather than fundamentals. December CPI was broadly in line with expectations, with some modest relief in core components, while BEIs continue to price inflation just over 2% through next year. This keeps inflation shocks a low-probability tail risk, with any upside pressure more likely to stem from geopolitical events than from structural demand or supply imbalances.

- AI momentum is fading as leverage risks move into focus. The AI theme softened modestly, with 2026 capex increasingly reliant on debt financing. This raises downside risk if enthusiasm wanes, as any leverage unwind could create outsized headwinds—given AI’s role as the primary driver of broad equity upside in 2025—and trigger a rapid risk-off regime.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- Is the current risk-on backdrop durable, or merely liquidity-driven? With geopolitics elevating risk premia, technicals largely flat, and quant sentiment only modestly recovering, markets appear supported more by policy accommodation and liquidity than by improving fundamentals—raising questions about sustainability if macro data disappoints.

- Does labor market data become the decisive regime-shift trigger in 2026? Cyclical leadership hinges on a soft-landing outcome, while meaningful labor weakness could accelerate easing expectations, favor growth and duration, and unwind cyclical positioning—making employment data the key swing factor across assets.

- Is AI transitioning from a growth tailwind to a systemic risk? As AI-driven capex becomes increasingly debt-financed, the theme’s dominance in 2025 raises the stakes for 2026: a slowdown or leverage unwind could propagate beyond tech and trigger a broader risk-off episode across equities and credit.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses highlights a market cautiously leaning risk-on as investors position around the FOMC. Republican policy-linked sectors and rate-sensitive trades are seeing renewed inflows, while cyclicals and defensives remain muted but improving, signaling a tentative shift in sentiment.

Markets undergo another volatile trading week as positive jobs data is overshadowed by Trump’s sweeping “Liberation Day” tariffs and consequential global retaliations.

This week we unpack the latest rout of market volatility, incited by trade frictions, waning risk sentiment, and monetary policy decisions.