Cautious Optimism Builds Ahead of FOMC Decision

Synopsis

This week’s Lenses highlights a market cautiously leaning risk-on as investors position around the FOMC. Republican policy-linked sectors and rate-sensitive trades are seeing renewed inflows, while cyclicals and defensives remain muted but improving, signaling a tentative shift in sentiment. With optimism creeping in but core positioning still conservative, the durability of this rotation hinges on whether Fed easing delivers more than just a tactical trade.

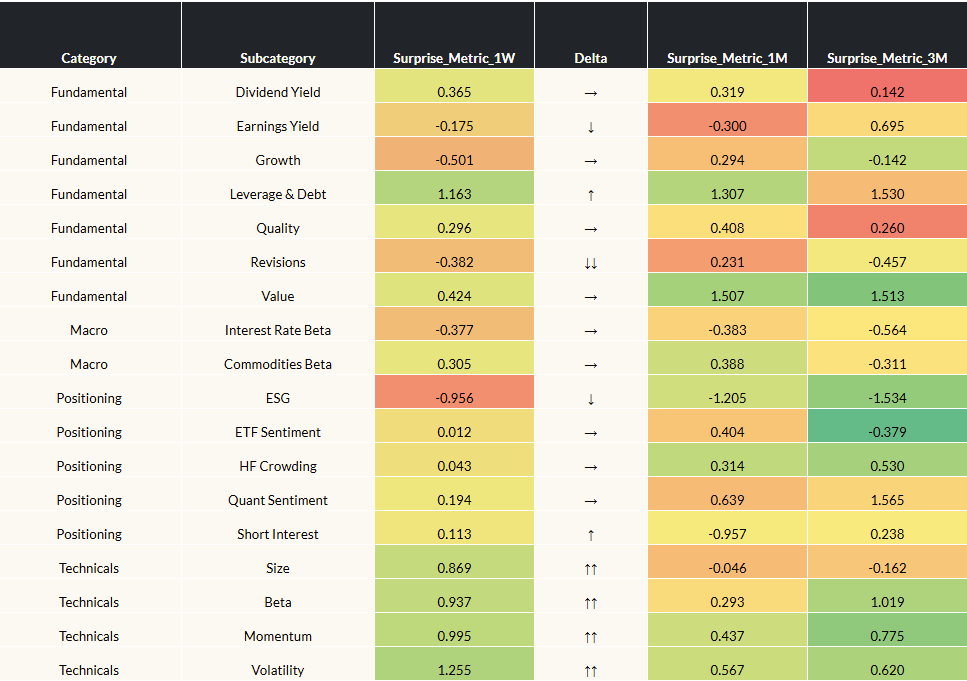

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 9/12/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Offense is the new defense. Markets shrugged off last week’s hot CPI and are squarely focused on the FOMC. A 25bp cut is baked in, but a surprise 50bp move would signal urgency on labor softness—likely accelerating flows into risk assets and amplifying cyclical factor gains.

- Cyclicals in charge. Momentum and Volatility are leading as investors lean into higher-beta exposures. Near-term positioning favors these risk-on factors, but the setup is vulnerable if Fed easing fails to match bullish expectations.

- Small caps in focus. Fundamental factors stayed muted, but leverage and debt-linked exposures popped on small-cap strength. A deeper cut would disproportionately benefit smalls given balance sheet sensitivity, though inflation flare-ups could quickly turn them from leader to laggard.

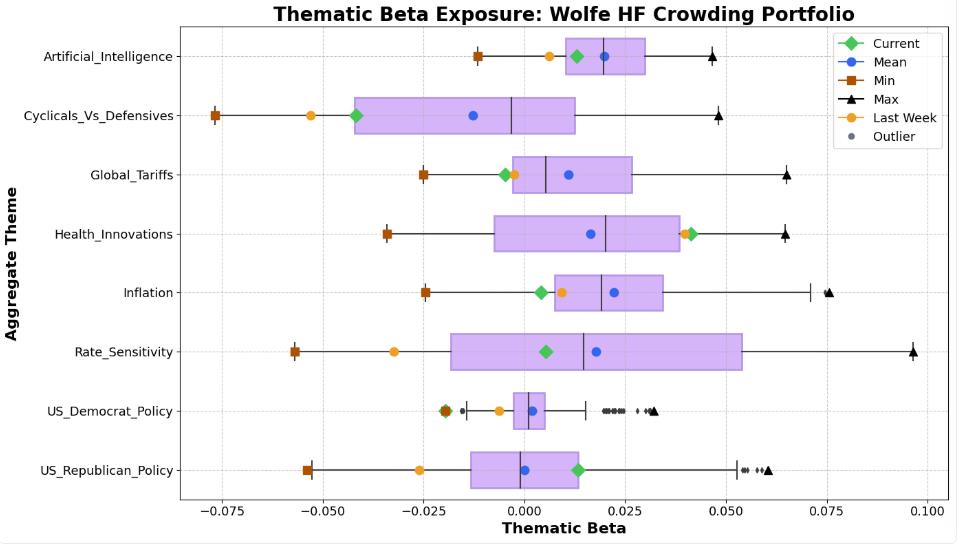

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Republican Policy theme bounces. Institutional flows turned positive into this theme suggesting investors are tactically leaning into areas like manufacturing and industrial sectors that could stand to benefit from a dovish Fed. The shift looks more like short-term positioning than a durable rotation.

- Cautious optimism. Cyclicals and Defensives remain net negative, underscoring conservatism in core positioning. Still, the week-over-week rebound hints at institutions probing for upside as policy clarity approaches.

- Rate sensitivity surges. Leveraged and rate-exposed names saw a strong boost as portfolios positioned for imminent cuts. The key question is whether these are tactical trades that roll off post-FOMC, or the start of longer-term bets on an extended easing cycle.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

Is Republican policy rotation tactical or durable?

Are institutions simply front-running dovish policy, or could this mark the beginning of a longer reallocation into policy-linked sectors?

Are rate-sensitive trades a fleeting bet—or the start of a cycle?

Leveraged and debt-heavy names rallied as portfolios positioned for cuts, but will these trades unwind post-FOMC, or extend into a broader easing play if labor softness forces the Fed’s hand?

Is cautious optimism enough to shift the market’s tone?

Cyclicals and Defensives remain negative overall, yet the rebound from last week suggests institutions are probing risk. Does this hint at a slow turn in sentiment, or just noise ahead of pivotal Fed guidance?

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

Markets are entering 2026 with elevated geopolitical risk but sustained risk-taking, supported by liquidity, policy accommodation, and still-contained inflation expectations. Leadership remains conditional: cyclicals benefit in a soft-landing scenario, while growth could reassert if labor data weakens and policy easing accelerates. At the same time, the market’s heavy reliance on AI-driven upside introduces a new fragility, where any leverage unwind could quickly shift sentiment to risk-off.

Markets undergo another volatile trading week as positive jobs data is overshadowed by Trump’s sweeping “Liberation Day” tariffs and consequential global retaliations.

This week we unpack the latest rout of market volatility, incited by trade frictions, waning risk sentiment, and monetary policy decisions.