Markets shift gears—less momentum, more margin of safety

Synopsis

This week’s Lenses point to a market caught between fading policy optimism and selective risk-taking. Investors are rotating out of expensive growth into cash-flow-rich cyclicals like Energy, while rate sensitivity and AI enthusiasm both moderate as the Fed’s path grows less certain. The common thread: positioning discipline is replacing momentum chasing as markets recalibrate to a higher-for-longer reality.

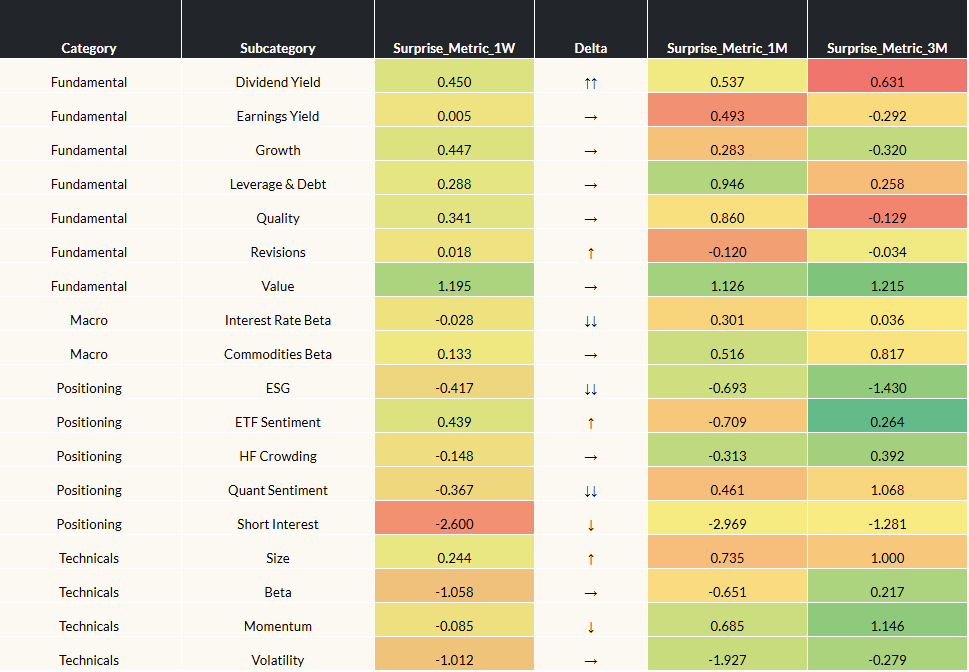

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 11/14/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Value resilience amid late-cycle rotation. Fundamental factor surprises were broadly flat, but the persistent outperformance of Value over Growth underscores continued investor preference for earnings visibility and balance-sheet strength. Leadership rotation toward Healthcare and Energy suggests markets are rewarding cash-generative defensives, while Quality exposure remains supported as retail participation and risk appetite cool.

- Momentum unwinds as policy clarity fades. Positioning factors were mostly negative, led by weaker Short interest and Quant sentiment. Momentum-heavy portfolios—still crowded in high-multiple Tech and Growth names—are vulnerable as the macro backdrop challenges duration trades. With rate-cut odds effectively a coin flip, a “hold” stance from the Fed could accelerate factor rotation away from Momentum toward Value and Quality.

- Labor data may redefine the Fed’s glide path. The government’s reopening brings a flood of delayed data, with labor reports front and center in shaping policy expectations. A sharp slowdown could push the Fed toward faster easing, boosting cyclical and duration-sensitive assets. But if job demand proves soft yet stable, the case for patience strengthens—favoring balanced risk allocation and selective de-risking rather than wholesale rotation.

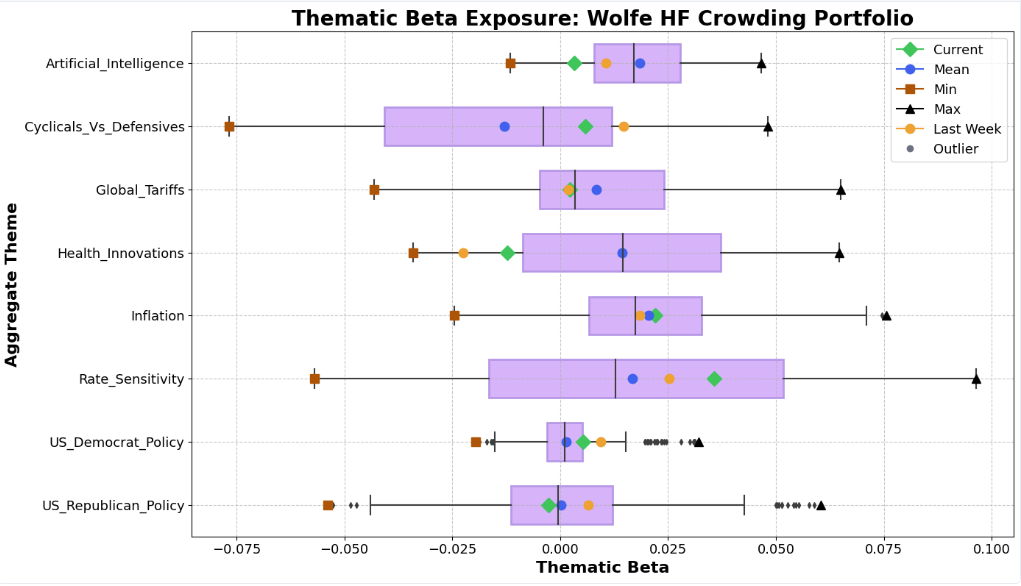

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Rate sensitivity back in focus ahead of the Fed. Institutions are positioning around the December FOMC with reduced conviction in near-term cuts but continued pricing for 2026 easing. If labor data hold firm, rate-sensitive assets could face repricing risk as the “policy cushion” narrative weakens.

- Cyclicals gain modest favor as flows rotate out of Tech. Rotation away from stretched Tech valuations has funneled capital toward Energy and other cash-flow-rich cyclicals. Hedge funds appear to be using Energy exposure both as an inflation hedge and a geopolitical buffer, suggesting a selective—not broad—risk-on posture.

- AI enthusiasm cools as valuations peak. AI beta has drifted toward neutral as investors digest rising capex and funding costs. While the structural story remains intact, crowded positioning and lofty multiples are constraining near-term alpha potential.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- Is the market too complacent on policy risk? Rate-cut odds have slipped, yet markets still price a generous easing path into 2026. If labor data prove resilient, the Fed may stay higher-for-longer—forcing a repricing across duration trades and rate-sensitive assets.

- Can cyclical leadership persist without a growth rebound? Flows into Energy and other high-cash-flow sectors signal selective risk-taking, but much of the bid reflects valuation support and inflation hedging rather than genuine growth conviction. Sustained leadership may require stronger real activity data.

- Are AI and Tech exposures entering a consolidation phase? With capex still rising but valuation enthusiasm fading, the AI complex may be transitioning from a narrative-driven trade to an earnings-driven one. The challenge now is finding alpha as leadership broadens and sentiment normalizes.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses highlight a barbell market, with renewed flows into both risk-on and defensive sectors, especially healthcare, energy, and financials, while fading tariff and trade themes signal recalibrating investor conviction ahead of pivotal macro and policy events.

Join us as we explore a week characterized by a surge in energy prices and historic levels of volatility across the International markets.

This week, we analyze equity markets stumbling into the second quarter alongside the stark disparities in sector allocations highlighted by Energy and Materials.