Markets Lean on Policy Hopes While Fundamentals Quietly Reset

Synopsis

This week’s Lenses explore a tension between policy-driven optimism and fundamental late-cycle realities. Rate-cut hopes, tariff shifts, and shifting inflation signals are driving rapid rotations—pulling investors toward cyclicals, under-owned sectors, and away from crowded Growth even as macro uncertainty remains unresolved. The common thread is a market increasingly led by policy expectations but priced by fundamentals, creating a fragile equilibrium where leadership can turn quickly.

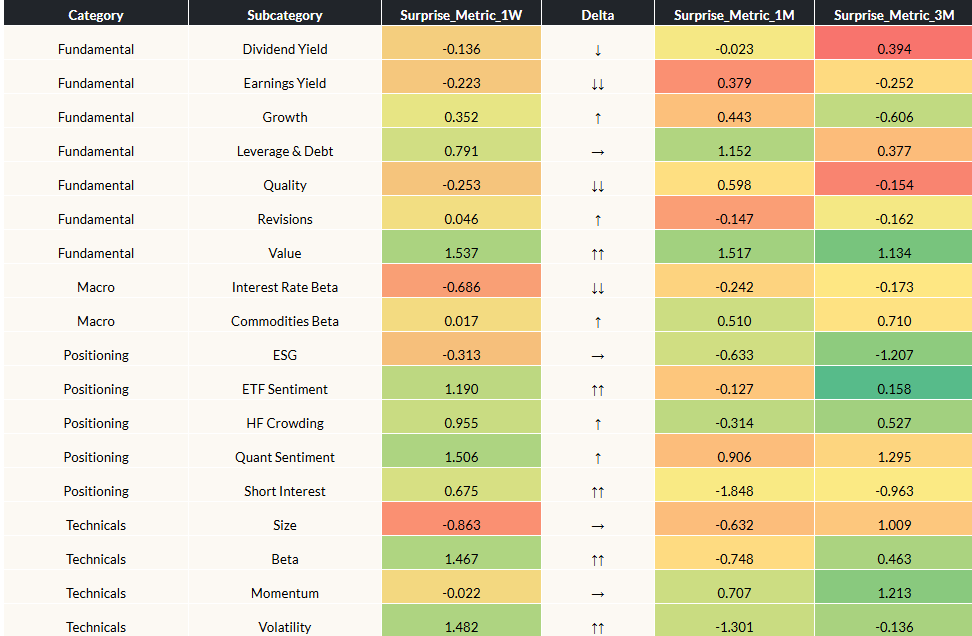

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 11/28/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- The Fed’s shifting tone is back in the driver’s seat, with rate-cut odds swinging to ~90% and fueling a rebound in risk assets after last week’s selloff. The tug-of-war between hawkish inflation concerns and dovish labor-market softness keeps duration and rate-sensitive exposures highly tactical.

- Easing expectations reignited a bid for Growth, Vol, and Beta, while defensive Quality and Earnings Yield lagged and Small Caps held steady—reinforcing that the market is willing to lean into cyclicality. Yet, on longer horizons, Value continues to deliver positive surprises, consistent with a late-cycle environment where fundamentals, not sentiment, are driving relative outperformance.

- Positioning metrics—Short Interest, Quant Sentiment, and Crowding—turned broadly supportive, echoing hedge funds’ growing allocations toward Health Care, Materials, and other under-owned sectors. This shift in leadership suggests investors may find better risk/reward in unloved cyclical and thematic pockets rather than crowded mega-cap growth.

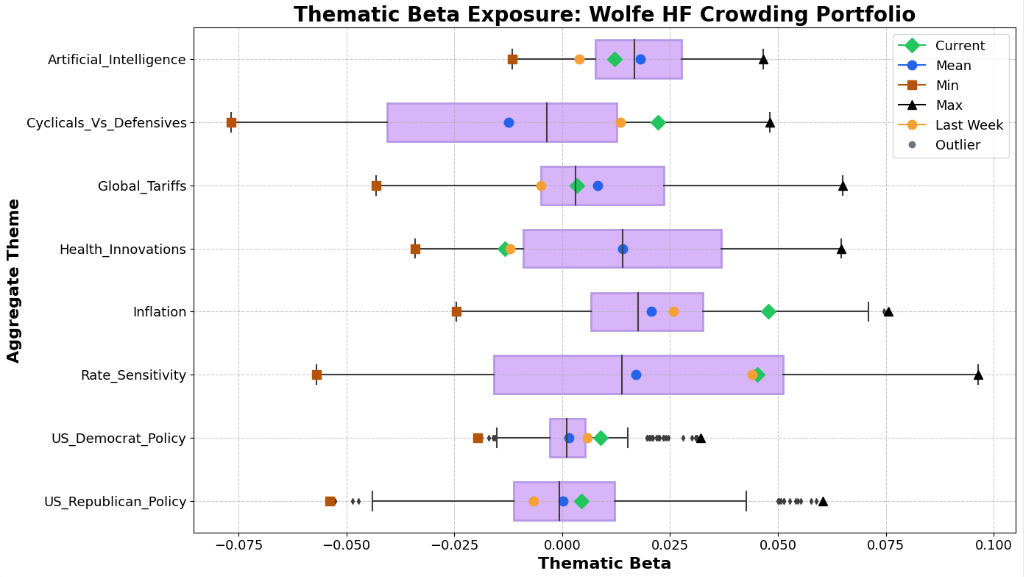

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Tariff beta is rising back toward historical averages, coinciding with the U.S. decision to extend exemptions on key Chinese industrial goods and the Supreme Court’s review of tariff authority. As trade headlines regain market relevance, investors should stay nimble in globally exposed cyclicals and watch supply-chain beneficiaries of any relief.

- Inflation has re-emerged as a portfolio-relevant theme, despite falling breakevens that sit below the Fed’s target. The sharp jump in Prices Paid—a leading indicator for PCE—signals upside inflation risk; any renewed pricing pressure would likely dampen rate-cut expectations and rotate leadership away from rate-sensitive Growth and Tech.

- Cyclical leadership continues to build, as hedge funds allocate toward Energy, Industrials, and Materials amid valuation fatigue in high-growth sectors. This rotation suggests that secular industrial themes—advanced manufacturing, infrastructure, and reshoring—may now offer superior risk-adjusted returns versus crowded, high-multiple Growth exposures.

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- Is the market underestimating policy risk at exactly the wrong time? With tariff sensitivity rising, U.S. trade policy back in motion, and inflation signals firming despite soft breakevens, investors may need to reassess whether policy-driven volatility (tariffs, Fed signaling, inflation surprises) could overpower the current risk-on tone.

- How durable is the rotation into cyclicals and under-owned sectors? Hedge-fund flows into Energy, Industrials, Materials, and select thematic areas suggest a genuine leadership shift—but it remains unclear whether this is a late-cycle catch-up trade or the front end of a more sustained rerating away from crowded Growth and Tech exposures.

- Are easing expectations doing more to distort positioning than fundamentals justify? Rate-cut hopes have powered Growth, Vol, and Beta, yet conflicting signals—rising Prices Paid, tactical rate sensitivity, small-cap resilience, and persistent Value outperformance—raise the question of whether investors are leaning too hard into an easing narrative that could quickly reverse.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses captures a market at an inflection point — where political realignment, sticky inflation, and shifting rate expectations are reshaping sector leadership.

Markets surged in May as easing trade tensions and cooling inflation bolstered investor confidence, though uncertainties around tariffs and economic growth persist.

Join us as we dive into a week of factor-neutral gains in both the US and International markets, as investors react to a week of corporate earnings news and hints at the policies that the new US president will pursue.