Tariffs, Policy Shifts, and a Market Searching for Direction

Synopsis

This week’s Lenses captures a market at an inflection point — where political realignment, sticky inflation, and shifting rate expectations are reshaping sector leadership. Despite the broader selloff, institutional investors remain selectively risk-on, rotating toward value, financials, and late-cycle cyclicals while defensives gain favor as rate cut hopes without official data have become murky at best. Meanwhile, Democratic policy momentum and evolving tariff dynamics inject both opportunity and uncertainty, reinforcing a market that’s trading more on policy nuance than macro clarity.

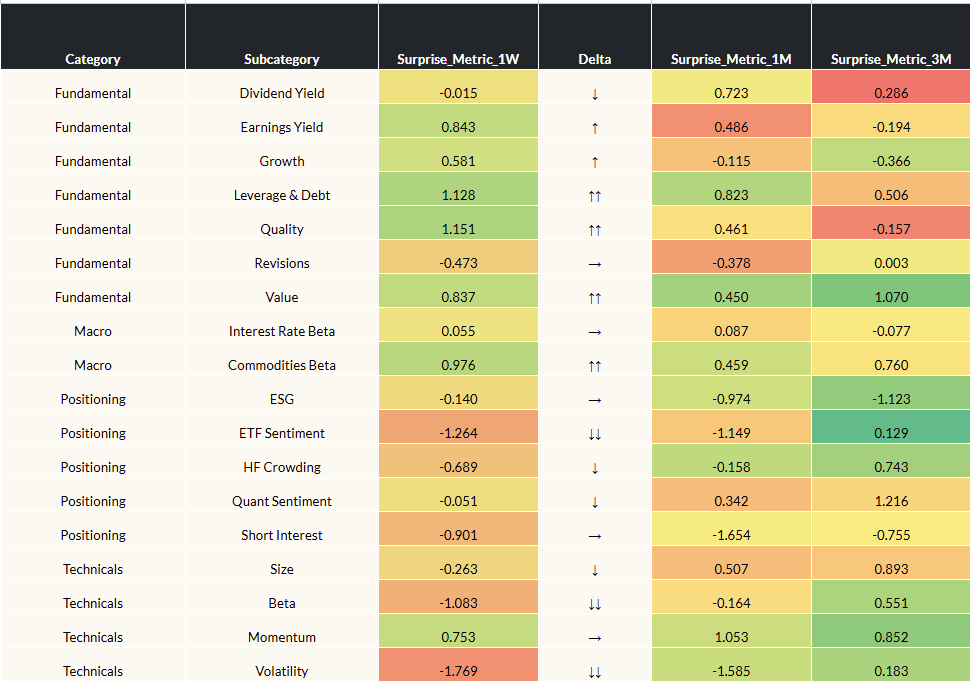

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 11/07/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Risk sentiment deteriorated: Weak consumer data and AI-bubble fears sparked a 3% Nasdaq decline, erasing roughly $800 billion in tech market cap, while Consumer Discretionary fell over 2%. Beta and Vol factors sold off sharply as investors rotated toward defensives — Quality and Earnings Yield factors strengthened, signaling a pivot back toward capital preservation and late-cycle positioning.

Policy outlook turned murky: The ongoing shutdown has disrupted key labor data and muddied Fed visibility, with December rate-cut odds slipping from 90% to ~64%. The market still prices roughly 75–100 bps of easing over the next 12 months, but uncertainty around timing keeps volatility elevated. A data deluge once the shutdown ends could reset expectations and spark yield repricing, especially in the 10-year, which has retraced toward 4.1%. - Rotation under the surface: Leadership shifted from Tech and Discretionary toward Energy (+3%) and Health Care (+2%), highlighting a broad rotation into value and defensives. Small caps and Growth remain most exposed if sentiment weakens further and the Fed turns hawkish. Investors may find more resilient opportunities in late-cycle value, quality balance sheets, and dividend yield exposures as markets adjust to a slower easing path.

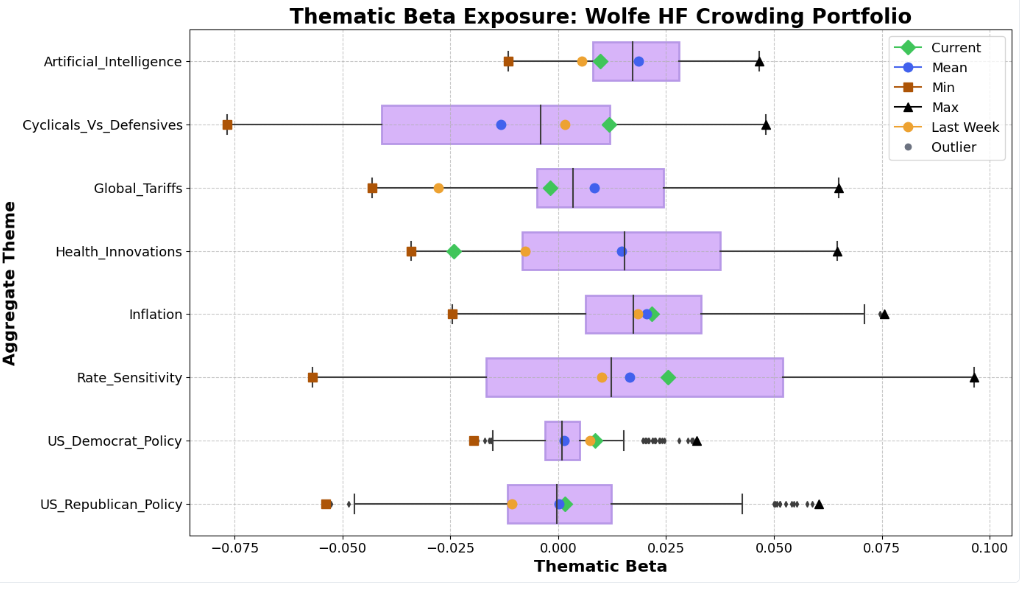

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Democratic policy resurgence reshapes sector tone: Blue-party wins last week revived thematic beta and expectations for classic Democratic beneficiaries like clean energy, infrastructure and healthcare spending. A renewed fiscal push in these areas could support late-cycle growth and catalyze rotation toward industrials, renewables, and public-works-linked equities, even as regulatory scrutiny for big tech and energy majors rises.

- Higher-for-longer rates recalibrate sector leadership: The Cyclicals vs. Defensives theme continues to climb, showing institutional portfolios remain tactically risk-on and contrarian to retail sentiment. But with market-based inflation expectations steady around 2.3–2.5%, the likelihood of the Fed continuing to cut past December is fading. That dynamic may disappoint rate-sensitive sectors like real estate and utilities, while benefiting banks, insurers, and late-cycle value plays that gain from a firmer rate backdrop.

- Tariff policy drives uncertainty but may alter margin dynamics: The Supreme Court’s challenge to tariff authority and talk of a $2,000 “tariff dividend” injected volatility into trade-linked assets. While potential tariff relaxation could ease input costs and lift corporate margins, new fiscal outlays may stoke inflation and deficit concerns. Investors should watch for renewed divergence between margin-sensitive equities (manufacturers, importers) and inflation beneficiaries (commodities, TIPS).

For Further Discussion

As you digest this week’s Lenses, consider further discussion on the following points:

- Will Democratic policy momentum reshape sector leadership?

Blue-party gains have revived classic themes like clean energy, healthcare, and infrastructure, but fiscal realities and implementation timelines will determine staying power. Investors should watch whether policy enthusiasm translates into earnings traction or fades as political momentum meets budget constraints. - Are higher-for-longer rates resetting market leadership?

With inflation expectations anchored around 2.3–2.5%, rate-sensitive assets face headwinds while banks and value sectors gain footing. If growth slows before inflation eases, the market may struggle to sustain risk-on positioning without clearer signals from the Fed. - Can tariff uncertainty reignite inflation or boost margins?

Legal and political debates over tariff authority, combined with the proposed “tariff dividend,” add a fresh layer of fiscal complexity. Whether these measures tighten supply chains or relieve cost pressures could shape both corporate profitability and inflation expectations into year-end.

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses explore a tension between policy-driven optimism and fundamental late-cycle realities. Rate-cut hopes, tariff shifts, and shifting inflation signals are driving rapid rotations—pulling investors toward cyclicals, under-owned sectors, and away from crowded Growth even as macro uncertainty remains unresolved. The common thread is a market increasingly led by policy expectations but priced by fundamentals, creating a fragile equilibrium where leadership can turn quickly.

Markets surged in May as easing trade tensions and cooling inflation bolstered investor confidence, though uncertainties around tariffs and economic growth persist.

Join us as we dive into a week of factor-neutral gains in both the US and International markets, as investors react to a week of corporate earnings news and hints at the policies that the new US president will pursue.