Market Concentration Deepens as Policy Path Grows More Complex

Synopsis

This week’s Lenses explores how the market’s rally has grown increasingly narrow, powered by momentum and megacap strength even as institutional positioning stays neutral/defensive. Tariff-driven inflation fears and uneven data have complicated the policy path, pulling long yields lower while leaving short-term rate expectations volatile. Beneath the surface, fading breadth and heightened concentration raise a central question: can this momentum-led advance endure without a clearer growth or policy catalyst?

Lens 1: Surprise Metric

Our “Surprise Metric” reveals factor movements outside of their historical return distributions for different horizons (Surprise 1W, 1M, 3M columns below). Values above 1 (below -1) standard deviation suggest outsized strength (weakness) relative to history (data sourced from our open ecosystem of risk model providers).

End Date: 10/10/2025

* Arrows represent directional change in 1W Surprise Metric. Single arrows indicate 1X or larger difference from previous week and double arrows indicate a 2X or larger difference. Horizontal arrows indicate minimal change.

Highlights

- Tariff volatility returns: Markets fell sharply Friday on renewed U.S.–China tariff headlines before rebounding Monday, echoing prior “TACO” playbooks. The speed of the recovery suggests investors still view trade shocks as transient, but the magnitude of the move exposes how thin liquidity and leverage can amplify volatility. Short-term traders remain highly reactive, while long-term allocators appear unfazed—implying more two-way risk around policy headlines than genuine trend change.

- Momentum extends leadership: Tech-led momentum strengthened further as AI and semiconductor names drew heavy inflows, widening the gap between thematic leaders and the broader market. Investors are now parsing whether surging AI capex can sustain earnings growth or risks front-loading returns. The increasingly interconnected “AI complex” — where suppliers, customers, and infrastructure providers overlap — makes it harder to distinguish durable growth from cyclical froth, keeping conviction concentrated in a narrow set of megacaps.

- Factor rotation reshapes leadership: Value’s decline against positive surprises in Growth and Size points to a rotation away from the “soft-landing, easing soon” narrative toward trades tied to structural innovation and large-cap balance-sheet strength. The move reinforces that investors are rewarding scalability and capital efficiency over cyclicality, even as higher yields challenge income and value exposures. Portfolio positioning remains asymmetric—momentum dominates leadership, while breadth and diversification continue to thin.

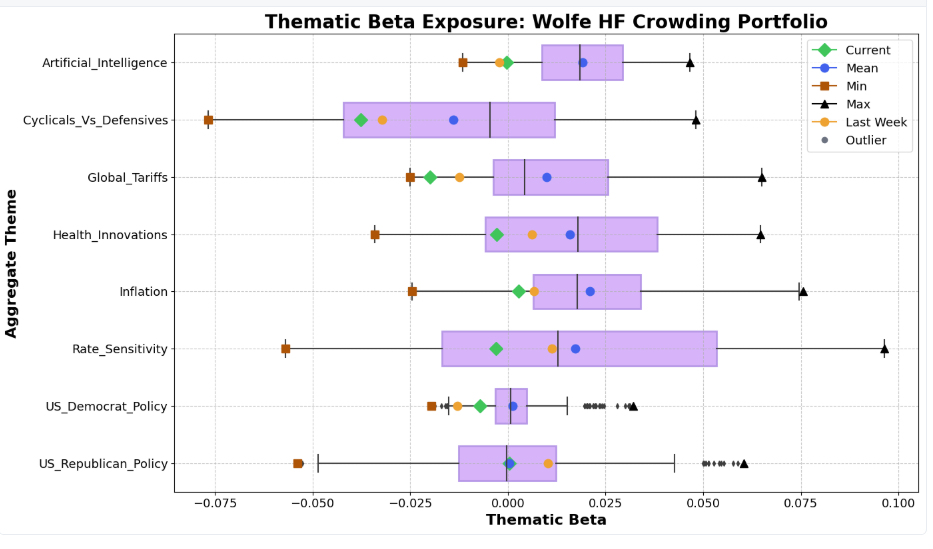

Lens 2: Thematic Crowding

This snapshot reveals thematic hedge fund exposure by measuring the beta of a Wolfe Hedge Fund Crowding factor portfolio to key market themes, calculated from residual return data. Higher beta indicates greater crowding in the theme, while lower beta suggests contrarian or avoided positioning to the theme. Data used for this analysis extends back to Jan 1st, 2024.

Highlights

- Institutions turn defensive: Most macro themes retraced last week as investors pared risk and rebuilt hedges. Rate sensitivity fell while Inflation themes firmed, reflecting renewed concern that tariff-driven price pressures or labor supply constraints could complicate the Fed’s easing path. With labor data still lagging due to the shutdown, proxy indicators hint at slowing payroll momentum—keeping conviction in policy-linked trades muted.

- Sentiment divergence widens: The Cyclicals-vs-Defensives theme edged lower, underscoring how institutional positioning remains cautious against headline-driven fiscal or policy rhetoric. Retail sentiment, by contrast, stays resolutely bullish—suggesting that retail and professional flows are increasingly disconnected in both direction and time horizon.

- Curve dynamics shift quietly: Markets continue to price softer growth, pulling long-term yields lower despite fiscal and policy-credibility risks. Inflation expectations, however, appear to be re-anchoring higher, implying a gradual bear-steepening may still be ahead as short rates fall faster than the long end in anticipation of Fed cuts.

For Further Discussion:

As you digest this week’s Lenses, consider further discussion on the following points:

Are institutions de-risking too early? With positioning turning defensive ahead of key labor data, could renewed easing momentum or improving earnings force another rotation back into rate-sensitive and cyclical exposures?

Can retail optimism outlast institutional caution? The widening sentiment gap raises the question of whether retail flows are a stabilizing force—or the next source of volatility if macro or policy headlines turn darker.

Is the curve’s message misread? Markets are pricing slower growth and earlier cuts, yet inflation expectations remain sticky. Does this imply the start of a structural steepening cycle—or a temporary repricing before policy credibility is tested again?

Omega Point can help you surface and explore these questions with data-driven clarity. Reach out if you'd like to dig deeper into any of these themes.

What Forces Are Impacting Your Performance? Find Out Now...

More Related Insights

This week’s Lenses highlight a shift toward Quality and Momentum factors amid cooling risk sentiment, with geopolitical tensions driving rotations into defensive assets. Hedge fund positioning shows reduced conviction in inflation and AI themes, with a growing focus on more durable macro narratives.

Join us this week as we explore a historically factor-driven week in the US markets highlighted by sharp reversals in Size and Momentum factors.

This week, we explore an uncertain economic landscape against the backdrop of positive quarterly economic reports.